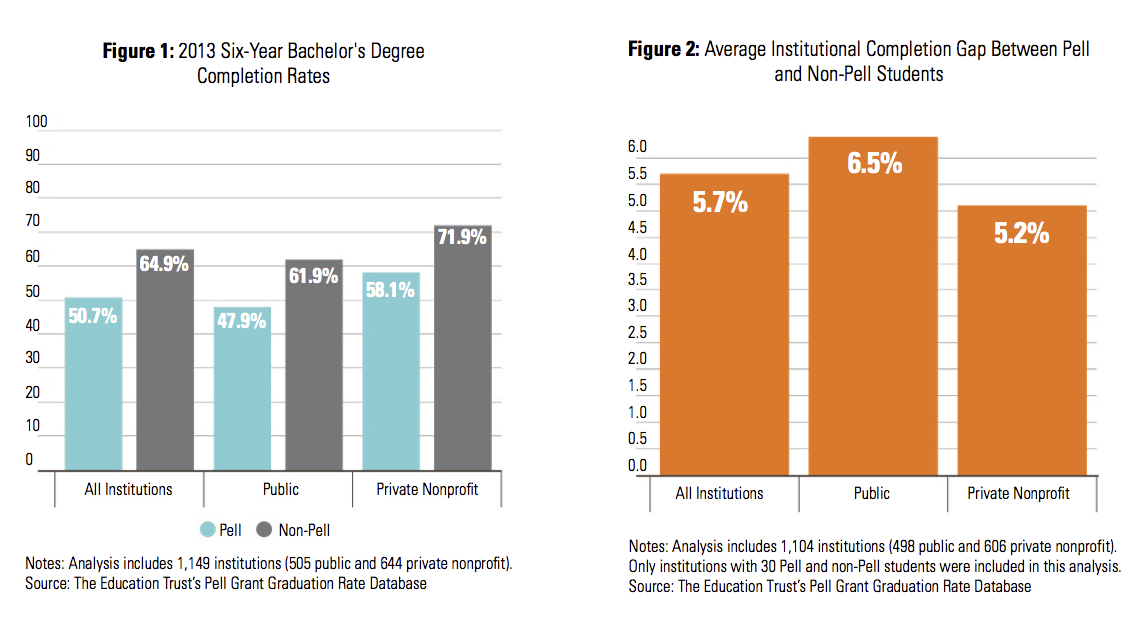

According to a new report by the Education Trust, the national graduation rate for Pell Grant recipients attending public and nonprofit private colleges and universities is considerably lower than the completion rate of non-Pell recipients: while almost 65 percent of non-Pell recipients graduate in six years, only half of Pell students leave with a bachelor’s degree in the same time frame.

This 14-point gap (which can be seen in Figure 1 above) is much larger than the average gap (of 5.7 percent) between Pell and non-Pell students who attend the same institution (see Figure 2).

How is this possible? This occurs because the national gap is more than the product of all the individual completion gaps between Pell and non-Pell students at colleges and universities. The national gap is also a byproduct of which institutions students attend, with Pell students much more likely to attend institutions with lower graduation rates for all students, and much less likely to attend institutions that graduate most of their students.

Update

The Education Trust refers to the university where I teach as “an ‘engine of inequality’ because very few students come from working-class and low-income family backgrounds, and it falls in the bottom 5% of all four-year colleges nationwide for its extraordinarily low enrollment of freshmen who receive Pell Grants, a type of federal financial aid for low-income students. This college is not very socioeconomically diverse.”