The story currently being peddled by the folks at Bloomberg [ht: ja] is that the American middle-class is currently suffering, as the enormous wealth they managed to accumulate during the past few years is now dwindling. And that crisis—the end of their “once-in-a-generation wealth boom”—is what they will take into the midterm elections.

There is a kernel of truth in that story but it is overshadowed by all that it leaves out.

The small sliver of truth?

Yes, as we can see in this chart, the average real wealth (in July 2022 dollars) of the middle 40 percent of Americans did in fact increase from January 2017 (when Donald Trump first took office) until March of 2022; now it has begun to fall and is projected to continue declining (according to data provided by Realtime Inequality).*

That should come as no surprise. It is the result of years of cheap money, which has fueled increases in the value of the two major components of middle-class wealth: house prices and the stock market. Now, while the price of real estate continues to rise (as anyone knows who has attempted to purchase a house in recent months), the stock market has taken a tumble (with the Fed policy of increasing interest-rates, on top of disruptions in global supply chains and the war in Ukraine).

So, yes, middle-class wealth is falling. But that’s only part of the what is going on out there, beyond Bloomberg’s narrow lens.

Another important part of the story, which I discussed on Wednesday, is the plight of the bottom 50 percent of American workers. Yes, their average wealth also increased during the same period but not by much more than a rounding error: a total of $13.8 thousand for each person. Their average wealth at the most recent peak reached $12 thousand, and not it too is beginning to fall.

What else is left out of the Bloomberg story? Well, it only refers to the absolute level of middle-class wealth.

As is clear from the chart above, the average wealth of the middle-class (the blue line) is much closer to that of the bottom 50 percent (the green line) than it is to the wealth of the top 1 percent (the brown line): $366.5 thousand compared to $11.9 thousand and $17.5 million, respectively. That doesn’t look like much of a bonanza to me, certainly not in relative terms.

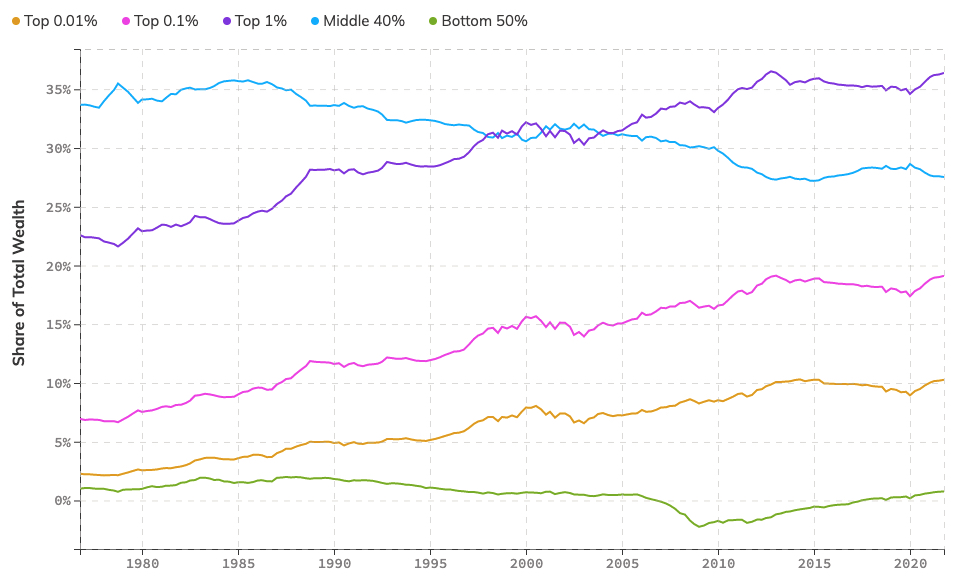

Indeed, the third major part of the missing story has to do with the changes over time in the shares of wealth owned by each of the the classes.

The fact is, the middle-class share of total wealth has been steadily declining since the mid-1980s (falling from 35.7 percent to 28.9 percent), while that of the entire bottom 50 percent has also decreased (from a minuscule 2 percent to a barely perceptible 1.2 percent). Meanwhile, the share of wealth owned by the top 1 percent has soared dramatically (from 21.8 percent to 34.6 percent).

If we add those three elements to Bloomberg’s story, we end up with a very different narrative about the U.S. economy. American workers—both poor and middle-class—have been losing out to those at the top for decades now.

Yes, along the way, there have been minor peaks and troughs in their accumulation of wealth (just as has been the case for those at the top) but the long-term trajectory is clear: a growing gulf between those at the top and everyone else. Under both Democratic and Republican administrations.

It’s a problem that will not be solved in this midterm election, not with the candidates and campaigns we’re seeing from both political parties.

It’s a fundamental problem with American capitalism. But that, alas, does not fit into the Bloomberg story either.

———

*The middle 40 percent is the population whose wealth falls between the 50th and 90th percentiles.

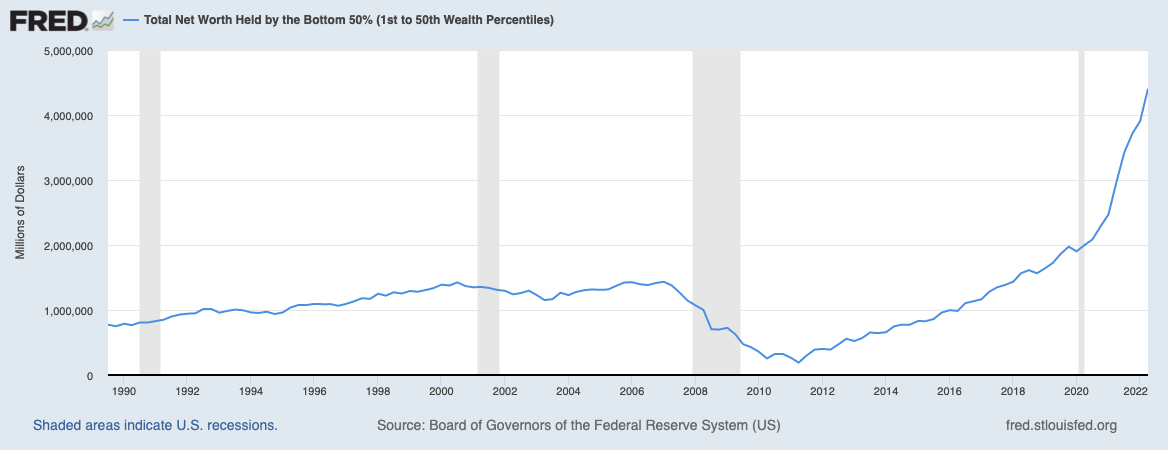

In a recent article in The Intercept, Jon Schwarz [ht: db] arrives at a perfectly reasonable conclusion—but, unfortunately, he makes a real hash of the data concerning changes in wealth ownership in the United States.

Schwarz starts with the fact that the total amount of wealth owned by the bottom 50 percent of the U.S. population has doubled since the first quarter of 2020 (in other words, during the pandemic). He then takes issue with the idea that economic growth needs to be slowed (for example, by the Fed’s raising of interest-rates) in order to help the poorest who presumably have been most hurt by inflation. And his conclusion?

According to the actual numbers, these are good times for many, many Americans in the poorer 50 percent. That doesn’t mean that millions aren’t struggling, but the financial prospects for most were even worse in the past in a lower-inflation world, a situation that did not excite the warm concern of the corporate media. What we should concentrate on now is keeping the streak going, not bludgeoning the workforce into submission.

I agree, at least in part: what policymakers are attempting to do (in a move supported by mainstream economists, large corporations, and the top 1 percent) is to bludgeon workers into submission. And there’s no reason to do so, especially when other policies—such as regulating prices, raising taxes on the rich, and imposing windfall profits taxes on large corporations—exist.

As for the rest of Schwarz’s argument, there are serious problems.

Let’s start with the idea that, in his view, these are good times for many Americans in the poorest 50 percent. This is based entirely on recent data concerning the net worth of those at the bottom has risen.

As is evident in the chart above, Schwarz’s claim about the rising wealth of the bottom 50 percent (the blue line) is in fact correct. It has been going up in absolute terms for more than a decade (since 2011), and it has gone up particularly quickly in the past two years.

Here’s the problem: the rising net worth of the bottom 50 percent is almost entirely due to the increase in housing prices (which therefore raises the net worth of those who own houses). But that doesn’t say anything about how well-off they are. They don’t get any extra income from those higher-priced homes. They therefore can’t purchase more or better commodities. And they can’t sell their homes to buy other ones because the other ones will also have increased in price.

So, that part of Schwarz’s argument doesn’t hold water. An increase in net worth based on higher housing prices doesn’t improve the well-being of those in the bottom 50 percent.

There’s nothing to rest his case on in terms of the absolute amount of wealth. What about in relative terms?

As it turns out, the increase in the net worth of the bottom 50 percent (again, the blue line in the chart immediately above) does lead to an increase in its share of total net worth—but only by 1 percent point, from 1.8 percent to 2.8 percent. It’s still below the share it had two decades ago. It only looks like an improvement because the share had fallen so low (to 0.3 percent, in 2011).

And compared to the top 1 percent (the red line in the chart)? The gulf between their respective shares has actually risen in the past two years. As of the first quarter of 2022, the share of total worth of the top 1 percent was 31.9 percent compared to the tiny (2.8-percent) share of the bottom 50 percent.

So, the bottom 50 percent is no better off in terms of net worth either in absolute or relative terms. In fact, against what Schwarz argues, the last several years have in fact been an economic disaster for the bottom half of U.S. households. Whatever improvement they’ve seen in terms of net worth is a chimeric dream.

I want to make one final point about the issue of net worth, which is often treated synonymously with wealth (including by Schwarz). As I argued above, whatever tiny bit of wealth those at the bottom have is almost entirely in the form of their houses. They don’t own any real wealth—call it financial or business wealth—of the sort that would allow them to have any role in making decisions about their economy.*

The top 1 percent do in fact have such a role, because they are able to convert their share of the surplus into real wealth, which allows them both to get more distributions of the surplus (through, for example, their ownership of equity shares in businesses) and to make the decisions (through their positions within those businesses, the financing of political campaigns, and the like) that do determine the trajectory of the economy and economic policy-making.

I’m entirely on Schwarz’s side in terms of opposing the current bludgeoning of workers on behalf of the 1 percent. But the better argument, it seems to me, is not to say that things should continue as before because the poorest households in the United States were better off, but to show that American workers have increasingly been beaten down, in both absolute and relative terms, precisely because of the pandemic and the profoundly unequal terms of the economic recovery.

Enough is enough. We have to adopt alternative economic policies in the short term, policies that don’t transfer all the costs of inflation-fighting onto the backs of workers. And then imagine and create a radically different form of economic organization moving forward.

———

*As I showed back in 2018, the top 1 percent owned almost two thirds of the financial or business wealth, while the bottom 90 percent (not just the poorest 50 percent) had only six percent.

This was supposed to be the great reset. As the U.S. economy recovered from the Pandemic Depression, millions of jobs were being created, unemployment was falling, and the balance of power between workers and capitalists would shift toward wage-earners and against their employers.

That, at least, was the promise (or, for capitalists, the fear).

But greedflation has delivered exactly the opposite: workers’ real wages are barely rising while corporate profits are soaring. There’s been no reset at all. That’s exactly what was happening before the coronavirus pandemic hit, and that trend has only continued during the recovery. It should come as no surprise then that the already grotesque levels of inequality in the United States continue to worsen.

And who are the beneficiaries? According to a recent study by the Institute for Policy Studies, it’s the Chief Executive Officers of American corporations who have managed to capture a large share of the resulting surplus.

Especially the CEOs of the largest low-wage employers in the United States. While median worker pay increased by 17 percent last year, CEO compensation rose by 31 percent. The result was that the ratio of CEO to average worker pay rose by 11 percent, to 670 to 1!*

American workers are struggling with rising prices, having risked their lives and livelihoods throughout the pandemic. Now, they’re forced to watch as their corporate employers, who have benefited from federal contracts and used their profits to buyback stocks, reward their CEOs with lucrative contracts and massive bonuses—far exceeding the small amount some workers have been able to claw back.

Who’s at the top? Amazon leads the list. Its new CEO, Andy Jassy, raked in $212.7 million last year, which amounts to 6,474 times the pay of Amazon’s median 2021 worker. Then there’s Estee Lauder’s CEO, Fabrizio Fred, who managed to secure a 258-percent pay increase in 2021—leading to compensation that amounted to 1,965 times that of the average worker. Third on the list was the CEO of Penn National Gaming, Jay Snowden, whose $65.9 million payout was 1,942 times that of the gambler’s typical worker’s wage.

So, how did they manage to capture so much surplus and distribute it to their CEOs? Like the other firms in the study, they all took the low road, paying their employees a pittance (in the low $30,000s for the median worker). And they’ve mostly succeeded in opposing and undermining union-organizing efforts.** But Amazon is the only one of the three to secure large federal contracts (over $10 billion between 1 October 2019 and 1 May 2022), like other low-wage corporations (such as Maximus, at $12.3 billion and TE Connectivity, at $3.3 billion), which means the taxes paid by ordinary Americans and being used to support such an inequitable corporate order.***

The report also highlights the extent of stock buybacks—which serve to inflate the value of a company’s shares and thus the value of executives’ stock-based compensation—among firms where median worker pay did not keep pace with inflation in 2021. Thus, for example, Lowe’s, the home-improvement chain, spent more than $13 billion in purchasing its own stock while median worker compensation fell by 7.6 percent to $22,697. Similarly, both Target and Best Buy increased workers’ pay by less than the rate of inflation but still spent millions of dollars in stock buybacks ($7.2 billion and $3.5 billion, respectively). In each case, a windfall to stock owners—including the CEOs—came at the expense of raises for the employees. For example, if the funds Lowe’s used to buyback its own stock had been divided among the company’s 325,000 employees, each worker would have received a $40,000 bonus.

Clearly, this economic order needs a fundamental reset.

And most Americans agree. According to a recent survey by Just Capital (pdf), more than eight in 10 respondents (83%) agree that the growing gap between CEO compensation and worker pay is a problem in the United States today. Moreover, according to the authors,

The message from the public is clear: responsibility lies with corporate leaders – including chief executives – to address income inequality in America today. Closing the gap requires action at the highest and lowest rungs of the corporate ladder.

The IPS suggests a range of options for doing something about the problem, including giving corporations with narrow pay ratios preferential treatment in government contracting, an excessive CEO pay tax, and a ban on stock buybacks (in addition to a wide variety of CEO pay reforms). If enacted, all such changes would serve to nudge such corporations out of the low road of poor worker pay and high CEO compensation and reduce the now-obscene level of inequality in the U.S. economy.

But giving employees a say in how those corporations are managed and operated would do even more to change the balance of power, within those firms and the entire economy, between workers and capitalists. The workers would then be able to participate in deciding how much surplus there would be and how it would be utilized—not only for their benefit but for the society as a whole.**** Employees would then become or participate in choosing the corporate leaders, including chief executives, who could actually go a long way toward solving the problem of inequality in America today.

That, in my view, is a reset of the U.S. economy worth imagining and enacting.

———

*Forty-nine of the 300 firms analyzed by the Economic Policy Institute had ratios above 1000-1. And, in 106 companies in their sample, median worker did not keep pace with the 4.7 percent average U.S. inflation rate in 2021.

**Amazon has spent millions of dollars in fighting union campaigns and, to date, have lost only one battle, in a Staten Island warehouse. (That’s in the United States. Some Amazon warehouses in Europe are unionized, with strikes being most frequent in Germany, Italy, Poland, France and Spain.) None of Estee Lauder’s U.S. workers have union representation, and less than 20 percent of Penn’s employees are unionized.

***Of the 300 companies in the IPS study, 119 — 40 percent — received federal contracts, totaling $37.2 billion. Their average CEO-worker pay ratio was 571-to-1 in 2021.

****Even Thomas Piketty now defends the idea of workplace democracy or co-determination, since workers “sometimes, they are more serious and committed long-run investors than many of the short-term financial investors that we see. And so getting them to be involved in defining the long-run investment strategy of the company can be good.”

Inflation continues to run hot—and now, finally, the debate about inflation is heating up.

On one side of the debate are mainstream economists and lobbyists for big business, the people Lydia DePillis refers to as having a simple mantra: “Supply and demand, Economics 101.” In their view, inflation is caused by supply and demand in the labor market, which is allowing workers’ wages to increase at an unsustainable rate (a story that, as I showed in April, has no validity), and supply and demand in the economy as a whole, with too much money chasing too few goods.

Simple, straightforward, and. . .wrong.

Fortunately, there’s another side to the debate, with heterodox economists and progressive activists arguing that increasingly dominant corporations are taking advantage of the current situation (the pandemic, disruptions in global supply-chains, the war in Ukraine, and so on) to jack up prices and rake in even higher profits than they’ve been able to do in recent times.

Josh Bivens, of the Economic Policy Institute, has offered two arguments that challenge the mainstream story: First, while “It is unlikely that either the extent of corporate greed or even the power of corporations generally has increased during the past two years. . .the already-excessive power of corporations has been channeled into raising prices rather than the more traditional form it has taken in recent decades: suppressing wages.” Second, inflation can’t simply be the result of macroeconomic overheating. That would suggest, at this point in a classic economic recovery, that profits should be shrinking and the labor share of income should be rising. As Biven notes, “The fact that the exact opposite pattern has happened so far in the recovery should cast much doubt on inflation expectations rooted simply in claims of macroeconomic overheating.”*

So, we have dramatically different analyses of the causes of the current inflation, and of course two very different strategies for combatting inflation. The mainstream policy (as I also wrote about in April) is to slow the rate of growth of the economy (for example, by raising interest rates) and increase the level of unemployment, thus slowing the rate of increase of both wages and prices. And the alternative? Bivens supports a temporary excess profits tax. Other possibilities—which, alas, are not yet being raised in the debate—include price controls (especially on commodities that make up workers’ wage bundles), government provisioning of basic wage goods (including, for example, baby formula), and subsidies to workers (which, while they wouldn’t necessarily lower inflation, would at least make it easier for workers to maintain their current standard of living).

What we’re witnessing, then, is an important debate about the causes and consequences of inflation. But, as DePillis understands, the debate is about much more than that: “The real disagreement is over whether higher profits are natural and good.“

In the end, that’s what all key debates in economics are about. Profits are the most contentious issue in economics precisely because the analysis of profits reflects both a theory and ethics about two things: whether capitalists deserve the profits they capture and what they can and should do with those profits. For example, profits can be theorized as a return to capital (and therefore natural and fair, as in mainstream economics) or they are the result of price-gouging (and therefore social and unfair, as in Bivens’s theory of corporate power).**

Similarly, capitalists can be seen as investing their profits (and therefore making their firms and the economy as a whole more productive, with everyone benefitting) or they can distribute a significant portion of their profits toward other uses (such as pursuing mergers and acquisitions, engaging in stock buybacks, and offering higher dividends, which do nothing to increase productivity but instead lead to more corporate concentration and make the distribution of income and wealth even more unequal).

Mainstream economists and capitalists have long sought to convince us that profits are both natural and good. In other words, when it comes to corporate profits and escalating charges of “greedflation,” they prefer to see, hear, and say no evil. The rest of us know what’s actually going on—that corporations are taking advantage of current conditions to raise prices, both to increase their profits and to lower workers’ real wages. We also know that traditional attempts to contain inflation through monetary policy will hurt workers but not their employers or the tiny group that sits at the top of the economic pyramid.

It’s clear then: the debate about inflation is actually a debate about profits. And the debate about profits is, in the end, a debate about capitalism. The sooner we recognize that, the better off we’ll all be.

———

*Even the Wall Street Journal admits that the wage share is not in fact growing: “The labor share of national output is roughly where it was before the pandemic.” Moreover, the current situation represents just a continuation of the trend of recent decades: “Over the last two decades. . .the share of U.S. income that goes to labor has fallen, despite periods of low unemployment.”

**Corporate profits can also be theorized as the result of exploitation (and thus a different kind of social determination and unfairness, as in Marxian theory).

There’s been a lot of talk about oligarchs these past couple of months. Russian oligarchs, that is—the billionaires who have accumulated vast amounts of wealth, including large stakes in Russian industries, mines, and banks, as well as superyachts, private jets, investment accounts, and real estate in the West. We’ve even learned their names: Vladimir Potanin, Leonid Mikhelson, Alexey Mordashov, and so on.*

They’re a pretty easy target, given Russia’s savage war on Ukraine. But what about the other oligarchs out there, why aren’t we talking about them? They also capture and keep massive amounts of the surplus produced by workers around the globe, and then accumulate even larger amounts of wealth, which they can live off of and utilize as they see fit. Why aren’t they on our radar?

Oh, they do pop up periodically. When Telsa founder Elon Musk engages in a hostile takeover of Twitter or workers manage to organize a union in one of Jeff Bezos’s Amazon warehouses or Michael Bloomberg decides to run for president. But there’s really no sustained attention paid to them or how they have managed to become billionaires. Which is why ProPublica’s recent investigation into the finances of the wealthiest Americans is so important.

The report is the latest in a series ProPublica started in June 2021 that examines the tax records of the top 0.001-percent wealthiest Americans—400 individuals all of whom earn more than $110 million a year.** In this installment, they show that U.S. oligarchs contrive to pay taxes at a lower rate than other Americans, even very wealthy ones just below them on the economic pyramid, for two reasons: first, because much of their income is derived from investments, like stocks, which is taxed at a lower rate; and second, they are able to use large charitable donations to obtain huge deductions. Most American workers don’t own much in the way of stocks, and their gifts to charity do little to lower their taxable incomes.

So, who are these oligarchs? Some of them (10 of the top 15) are tech billionaires, whose incomes generally came from selling stock—including the usual suspects like Bill Gates, Jan Koum, and Larry Ellison. About one fifth of the top 400 earners are managers of hedge funds—with names perhaps less familiar for those of us outside financial circles, people like Ken Griffin, Jeffrey Yass, and David Siegel—whose income comes from trading stocks, options and other financial instruments that flows directly to them. Executives and founders of private-equity firms also stand out: people like Stephen Schwarzman, Stephen Feinberg, and George Roberts, who generally make their money by buying companies and reselling them for a profit. And then there are the heirs of large fortunes, including the eleven heirs of Walmart founders Sam and Bud Walton and four of Amway founder Richard DeVos; these inheritors of great wealth generally receive their income from dividends or other forms of investment income.

All of them, in one way or another, have figured out how to capture portions of the surplus produced by workers in the United States and around the world. They’re not necessarily capitalists (in the sense of directly appropriating the surplus through a process of exploitation)—although some of them clearly are, such as Jeff Bezos (who sits on and is the Executive Chairman of the board of directors of Amazon)—but they do occupy positions that allow them to capture distributions of the surplus produced and appropriated by others. And they did quite well in sharing in the capitalist booty: each of the top eleven averaged over $1 billion in income annually from 2013 to 2018!

Not only do these oligarchs manage to capture distributions of the surplus. As ProPublica explains, they also get to keep a higher portion than many other wealthy people. Thus, for example, the top 400 paid an average tax rate of 22 percent, while those who “only” took home $2-5 million were taxed at a higher rate, 29 percent. In other words, those in the top 400 (and their armies of accountants and financial advisers) have managed to find the “sweet spot” of high incomes and low taxes.

How do they manage to do that? One reason is because much of their income is derived from business investments, not wages or salaries, and in the United States income from financial assets (including, starting in 2003, most stock dividends) is generally taxed at a lower rate.*** Thus, the top 400 saved an average of $1.9 billion in taxes each year—due solely to the lower rate on dividends. The second reason is because U.S. oligarchs often take huge charitable deductions that reduce their income subject to tax. A particularly generous provision of the U.S. tax code allows them to deduct the full value of any stock they donate at its current price—without ever having to sell it and pay capital gains tax. According to ProPublica,

Those two factors—the amount of income taxed at the advantageous rate and the ability to muster large deductions—are the main drivers of lower tax rates for those with the highest incomes.

Now, of course, that 22-percent tax rate is still much higher than the 5-percent effective income tax rate on people who earn $40-50 thousand per year. Except. Workers actually pay more in taxes for Social Security and Medicare than income taxes. The oligarchs, meanwhile, tend to pay proportionally little of these types of taxes because wages are a tiny portion of their total incomes. Factor those payments in and the rates are almost equal: a 21-percent total tax rate for a single worker earning $45 thousand and 23 percent for those in the top 400 (by income).****

The U.S. tax system is often referred to as progressive, meaning the tax rate rises the further you go up the income ladder. As it turns out, it is anything but. The few at the top who occupy positions that allow them to receive distributions of the surplus end up paying taxes at just about the same rate as all those people at the bottom who actually work for a living.

And the result of U.S. oligarchs’ ability to capture and keep their share of the surplus? Well, the gap between them and workers at the bottom of the economic pyramid continues to grow.

As is clear from this chart, the shares of pre-tax national income captured by those in the top .001 (the red line in the chart) and bottom 50 percent (the blue line) have been steadily moving in opposite directions since 1980. And the linear trend lines show that their respective shares continue to diverge. By 2021, the oligarchs’ share had soared to 1.7 percent, while the share of all the workers in the bottom 50 percent had fallen to 13.6 percent.

And the American oligarchs’ response to criticisms of this obscene inequality? Well, at least one of them—Musk, during a fawning interview with Chris Anderson, the head of Ted—offers a simple response: “At this point, it’s water off a duck’s back.”*****

———

*The fifth-richest man in Russia, Alisher Usmanov, owns Dilbar, the largest motor yacht in the world by gross tonnage. The boat is 512-feet long and reportedly cost $800 million, employing 84 full-time crew members.

**Just to put things in perspective, a typical American worker making $40,000 a year (a dot smaller than a pixel in the chart at the top of the post) would have to work for 2,750 years to make what the lowest-earning person in this group made in just one.

***Since 2013, the long-term capital gains tax rate has been 20 percent, just under half the top rate on ordinary income (37 percent in 2018).

****The tax rate for the 25 richest oligarchs (by wealth) is even lower: just 16 percent.

*****Musk’s income tax bill in 2018 was exactly zero. He responded to ProPublica’s request for comment with a lone punctuation mark—“?’’—and did not answer any detailed follow-up questions.

Everyone knows that inflation in the United States is increasing. Anyone who has read the news, or for that matter has gone shopping lately. Prices are rising at the fastest rate in decades. The Consumer Price Index rose 8.6 percent in March, which is the highest rate of increase since December 1981 (when it was 8.9 percent).

Clearly, inflation is hurting lots of people—especially the elderly living on fixed incomes and workers whose wages aren’t keeping up the price increases. No mystery there.

The only real mystery is, what’s causing the current inflation? That’s where things gets interesting.

To listen to or read mainstream economists the answer to the whodunnit is workers’ wages. They’re going up too fast, because the level of unemployment is too low and their employers are forced to pay them higher wages. As a result, corporations are compelled to raise their prices. Therefore, something has to be done (like increasing interest rates) to slow down the economy and force more workers into the Reserve Army of the Underemployed and Unemployed.*

The U.S. economy still looks overheated. Rising wages are a good thing, but right now they’re rising at an unsustainable pace. . .

This excess wage growth probably won’t recede until the demand for workers falls back into line with the available supply, which probably — I hate to say this — means that we need to see unemployment tick up at least a bit.

The amazing thing about Krugman’s story, and that of most mainstream economists, is there’s not a single word about profits. Corporate profits are entirely missing from their story. Inflation is only caused by workers’ wages, not the surplus raked in by U.S. corporations. Which is pretty amazing, given the numbers.

A quick look at the chart at the top of the post shows what’s been going on in the U.S. economy. Workers’ wages (the red line in the chart, the hourly wages of production and nonsupervisory workers) rose during 2021 at an annual average rate of less than 5 percent (ranging from 2.8 percent in the second quarter to 6.4 percent in the final quarter).

And profits? Well, they’ve been growing at astounding rates, magnitudes more than wages. Corporate profits (the light green line) rose during 2021 at an average rate of 40 percent, and the profits of nonfinancial corporations (the dark green line) expanded by even more: 69 percent!

Hmmm. . .

The fact that profits are entirely missing from the mainstream story about inflation reveals a fundamental problem within mainstream economic theories. On one hand, in their macroeconomics, wages and not profits are always the culprit. That’s because they only have a labor market, and not a capital market (much less a profit rate or, for that matter, a rate of surplus-value), when they analyze fluctuations in prices and output. It’s as if corporate profits are only a residual—what is left over in the difference between wages and wage-driven prices. On the other hand, in their microeconomics, profits represent the return to capital, and thus a key component of commodity prices as well as the driver of economic growth.

Such “capital fetishism” means that profits as the return to a thing, capital, play an important role in the mainstream theory of value but then disappear entirely in the macroeconomic story about inflation.

It’s therefore a problem in the basic theories of mainstream economics. And it’s a problem when it comes to their economic policies: anything and everything must be done to keep workers’ wages in check, and (without ever mentioning them) to safeguard corporate profits.

The fact is, once we solve the mystery of the missing profits we can actually tackle the problem of inflation. But neither mainstream economists nor the leaders of corporate America are going to like what we come up with.

___

*The Federal Reserve is suggesting that it can raise interest rates to get prices down “without causing a recession.” In fact, according to research from the investment bank Piper Sandler, the Fed raised rates to combat inflation nine different times during the past 60 years, and on eight of those occasions a recession occurred not long after.

In the world according to Paul Krugman, “most Americans” have gotten considerably richer over the past two years (even if “the gains have been especially big at the top”), “lower-income Americans [have] seen relatively large income gains,” and “the simple story that the pandemic has been great for the wealthy and bad for the working class doesn’t hold up.”

Really?

To support his argument, Krugman trots out a series of charts from Realtime Inequality, which is in fact an eye-opening set of statistics on wealth and income inequality in the United States. But not in the way Krugman uses them. The two biggest problems in Krugman’s treatment are (a) he excludes the bottom 50 percent (so that “most Americans” refers only to the middle 40 percent) and (b) he focuses on growth rates and not levels or shares of income and wealth (so that, once again, we have that pesky problem of large percentage increases on a low base yields small increases).

That’s how you lie with inequality statistics.

What happens if you look at other statistics? Let’s start with wealth.

Here, I’ve depicted the shares of wealth for various deciles of the U.S. population: top 0.01 percent, top 0.1 percent, top 1 percent, middle 40 percent, and bottom 50 percent. Lo and behold, we can see that, starting in 1979, the shares of wealth held by those at the very top have soared, the share of the middle 40 percent has fallen, and the share of the bottom 50 percent hasn’t budged.

What about for the most recent period (which is what Krugman focuses on), from the end of 2019 to the end of 2021. Same thing: the shares of wealth of the top 1 percent (and subsets of that group) have continued to rise, the share of the middle 40 percent has fallen, and the share of the bottom 50 percent has actually risen.

Wow! The share of wealth owned by the bottom 50 percent (which consists mostly of housing they may own) has gone up. By how much? From a minuscule amount to another minuscule amount—from 0.3 percent to 0.8 percent. Or, in absolute terms, from an average wealth of $2.9 thousand to $7.9 thousand—a difference of $5 thousand. You might even say such an increase means a lot to the 125 million people in the bottom 50 percent of the U.S. population but it’s certainly no more than a drop in the bucket in terms of closing the gap with the wealth of those at the top (for example, the $19 million of wealth owned by those in the top 1 percent).

What about income? Same problem.

The growth rate of post-tax income for those in the bottom 50 percent was, in fact, much higher than for those in the middle 40 percent and top 1 percent—8.5 percent compared to 3.8 percent and 4.1 percent, respectively.

And that proves what? Not much. Those in the bottom 50 percent gained $2.8 thousand (mostly from transfer payments), which is similar to the gain for those in the middle 40 percent ($3.2 thousand). And those in the top 1 percent? Well, they managed to capture an extra $48 thousand during the period from late 2019 to late 2021.

So, sure, wages for those at the bottom are growing at a faster rate than those at the top. But they’re still barely staying ahead of inflation. And they’re not such as to even put a dent in the gap that separates them from the incomes captured by those at the top. The share of post-tax income taken home by all those workers in the bottom 50 percent only increased from 20.1 percent to 20.9 percent, while the share of income captured by the 2.5 million people in the top 1 percent is still 14.4 percent.

All of which means what? That the gap between workers at the bottom (including those in the middle) and the small group at the top continues to be enormous—in terms of both wealth and income. And no policy of keeping existing interest-rates or increasing them will help close that obscene gap.

It’s time we stop lying with inequality statistics and focus on the real culprit: all the ways contemporary capitalism, both before and during the pandemic, has managed to funnel most of the surplus to those at the top of the economic pyramid, leaving barely enough wealth and income to get by for everyone else.

It’s a “simple story,” with clear political implications. Maybe that’s the reason the Krugmans of the world don’t want to tell it. . .

You don’t have to read Marx to understand the lack of power workers have under capitalism. But you do have to read beyond mainstream economists and economic pundits. You might turn, for example, to the business school.

Yes, I know, that’s a strange assertion. But let me explain.

The usual argument these days is that workers have acquired a lot more power because of the scarcity of labor. When labor is scarce (basically, when the quantity supplied of labor is less than the quantity demanded), workers can fetch higher wages and be pickier about the jobs they’re willing to accept. That, of course, drives employers crazy and, as usual, mainstream economists and commentators just echo those concerns.

So, is it true? Well, look at the data they cite:

The blue line represents the number of job openings, while the red line is the number of unemployed workers. And, look, way over on the right-hand side of the chart the blue line is slightly higher than than the red line! (Numerically, there were 10.1 million job openings recorded at the end of June and 9.5 million unemployed workers.In other words, for every available 100 jobs, there are only 94 unemployed people available.) And that scares the bejesus out of employers and those who always take the side of employers: they might have to pay workers more to take the terrible, low-paying jobs they are offering.

The result is an increase in workers’ power, as Ben Popken explains:

A pandemic-tightened labor market has given willing and able workers more of an upper hand with their employers for the first time in generations. . .

Worker power is the ability of an employee to command higher wages and benefits and set terms about their working conditions.

Not so fast! Yes, some workers might benefit from the current tight labor market but certainly not all of them, especially at the bottom of the economic pyramid.

Moreover, as Julie Battilana and Tiziana Casciaro remind us, while “it’s understandable” that some claim that workers have more power now than they did during the worst months of the pandemic, it’s still the case that “power remains highly unbalanced in most American workplaces.”

In non-unionized, hierarchical organizations, it is still concentrated in the hands of top executives and shareholders who control all company decisions and priorities, from pay levels to hiring (and firing), and company strategy and policies. Workers continue to have no representation on most corporate boards of directors and have no or very little say over any of these decisions even though they affect their work lives and livelihoods. This lack of control has detrimental effects on worker health and well-being: It has been associated with job dissatisfaction, greater mental strain and damaged physical health. The philosopher Elizabeth Anderson has written that American “workplaces are small tyrannies,” resembling dictatorships more than democracies.

In other words, workers have two positions within capitalism: they sell their ability to work in markets for labor power and then, after those exchanges are concluded, they leave the market and enter another realm, where they perform labor. And inside the enterprises where they work, they have no power at all. There, in the realm of production, their employers—the corporate boards of directors or capitalists—have all the power. That’s why capitalists enterprises are dictatorships, not democracies.

And if workers did have power inside the enterprises—if, for example, the enterprises were organized instead as worker-owned cooperatives?

giving workers more power means giving them the right to collectively validate or reject important decisions that affect their work lives, including the choice of the CEO, how profits are shared, what strategies to pursue and what to prioritize in the face of a health crisis like the pandemic.

And if employers and mainstream economists don’t attempt “to reduce the extreme power imbalance that so clearly puts workers at a disadvantage”? Then, Battilana and Casciaro warn, workers might take matters into their hands:

when the distribution of rewards in an economic system is so unequal as to appear blatantly unfair, those with less power are more likely to upend the current system entirely.

That, of course, would mean the end of capitalism. . .

Both the number of initial unemployment claims for unemployment compensation and the number of continued claims for unemployment compensation are once again on the rise, signaling a worsening of the Pandemic Depression.

This morning, the U.S. Department of Labor (pdf) reported that, during the week ending last Saturday, another 935 thousand American workers filed initial claims for unemployment compensation. While initial unemployment claims remain well below the peak of about seven million in March, they are far higher than pre-pandemic levels of about 200 thousand claims a week.

The number of continued claims for unemployment compensation, while also below its peak, rose from the previous week and was more than 20.6 million American workers—a figure that includes workers receiving Pandemic Unemployment Assistance.* This means that, since the end of April, the number of continued claims has fallen below 20 million only once (and that to 19 million, toward the end of November).

To put this number into further perspective, consider the fact that the highest number of continued claims for unemployment compensation during the Second Great Depression was 6.6 million (at the end of May 2009), and in the week before the Pandemic Depression began there were only 1.6 million continued claims by American workers.

In the meantime, at least 1,074 new coronavirus deaths and 40,607 new cases were reported in the United States yesterday. As of this morning, more than 6.1 million Americans have been infected with the coronavirus and at least 185.6 thousand have died—more than any other country in the world, which has received barely a mention from anyone in the Trump administration.

According to Gregory Daco, chief U.S. economist at Oxford Economics, “We are not moving in the right direction. With the looming expiration of benefits, it’s even more worrisome.”

In the meantime, at least 3,611 new coronavirus deaths and 245,033 new cases were reported in the United States yesterday—two morbid new records. As of this morning, more than 17 million Americans have been infected with the coronavirus and at least 307,642 have died. That’s more than any other country in the world, a crisis continues to receive barely a mention from anyone in the Trump administration.**

The result will be new waves of business slowdowns and closures, which in turn will mean millions more U.S. workers furloughed and laid off. Widespread inoculations of the U.S. and world populations are still many months off. Therefore, in the absence of a radical change in economic policies and institutions, Americans can expect to see steady streams of both initial unemployment claims and continued claims in the weeks and months ahead.

———

*This is the special program for business owners, the self-employed, independent contractors, and gig workers not receiving other unemployment insurance.

**The last time I posted a chart of unemployment claims, in early September, some 6.1 million Americans had been infected with the coronavirus and 185.6 thousand had died.

In this post, I continue the draft of sections of my forthcoming book, “Marxian Economics: An Introduction.” The first five posts (here, here, here, here, and here) will serve as the basis for Chapter 1, Marxian Economics Today. The next six (here, here, here, here, here, and here) are for Chapter 2, Marxian Economics Versus Mainstream Economics. This post (following on two previous ones, here and here) is for Chapter 3, Toward a Critique of Political Economy.

The necessary disclosure: these are merely drafts of sections of the book, some rougher or more preliminary than others. I expect them all to be extensively revised and rewritten when I prepare the final book manuscript.

Utopian Socialism

The third major influence on Marx’s critique of political economy (in addition to and combined with classical economics and Hegel’s philosophy) was utopian socialism.

During the early to mid-nineteenth century, socialist ideas were sweeping across Western Europe—starting in France and Britain—and traveling from there to many other parts of the world. They provoked extensive discussions and debates, a wide variety of plans to ameliorate the ravages of capitalism and to replace it with something better, and not a few attempts to create a radically different economic and social order.

The idea of utopia can be traced back to to the sixteenth century, to Thomas More’s famous text of that name. But socialist versions of utopia came much later, in response to the frustrated promises of the French Revolution. The crises of the Ancien Régime, caused by obscene levels of social and economic inequality, provoked a demand for liberty, equality, and fraternity. But for all the upheaval in France—the breaking-up of the feudal order (including the stripping-away of the privileges of nobility and the breakup of large Church-owned estates) and the creation of radically new social and political institutions (such as the institution of universal [male] suffrage and the abolition of slavery in the colonies)—the initial revolution and the subsequent restoration, which combined to enshrine individual rights and private property, served to clear the way for capitalism and thus new forms of inequality.

Socialist ideas sprung up in response, inspired both by the utopian promises and by the failures in practice of the Revolution. They served as a counterpoint to the other utopia being offered at that time, that of the classical political economists, which celebrated the emergence of capitalism. The utopian socialists, in contrast, were critical of capitalism and its negative effects on workers and the wider society. The most interesting and influential of this latter group were, in France, Henri de Saint-Simon and Charles Fourier, and, in Britain, Robert Owen.

Saint-Simon claimed that the needs of the industrial class, which he also referred to as the working-class, needed to be recognized and fulfilled to have an effective society and an efficient economy.* He argued, in consequence, that the direction of society should be in the hands of scientists and engineers (not the “idling class,” who produce nothing but live off the labor of others), in order to allow for the rapid development of technology and industry (Industry, which appeared in 1816-17), and that religion “should guide the community toward the great aim of improving as quickly as possible the conditions of the poorest class” (The New Christianity, published in 1825).

Fourier, for his part, presented a more radical critique of the existing order and plan for creating a new kind of economic and social organization. Not only did he attack poverty as one of the principal disorders of society (which could be solved by raising wages and providing a basic income for those who could not work), he argued that labor itself (indeed, all creative endeavors) could be transformed into pleasurable activities (see especially Le nouveau monde industriel et sociétaire, ou Invention du procédé d’industrie attrayante et naturelle distribuée en séries passionnées [“The New Industrial World”], originally published in 1829).** The primary mechanism for this would be the formation of “phalanxes” (based upon buildings called phalanstères or grand hotels) that would encourage the cooperation of different kinds of labor (based on jobs chosen according to the interests and desires of their members), which would both raise productivity and create social harmony.

In Britain, it was Robert Owen who became best known for attacking the deplorable conditions in which factory workers lived and labored—blaming the conditions, not on workers themselves, for their plight. He then sought to change those conditions: first, in the New Lanark Mills in Scotland, which he owned and managed and where he improved working conditions as well as providing youth education and child care; and then on a much larger scale, as an avowed socialist (A New View of Society: Or, Essays on the Formation of Human Character Preparatory to the Development of a Plan for Gradually Ameliorating the Condition of Mankind, publishedin 1816), Owen advocated radical social reform (such as the formation of trade unions and the provision of free education for children) and proposed a model for the organization of self-sufficient communities to serve as the basis for a “new moral world” (which was also the name of a newspaper he started in 1834, which carried the subtitle “A London Weekly Publication. Developing the Principles of the Rational System of Society”).

During the first half of the nineteenth century, when Marx was developing and then extending into new areas his “ruthless criticism of everything existing,” and beginning his lifelong collaboration with Engels, these were the socialist ideas that were “in the air,” discussed and debated by a wide variety of thinkers and activists (socialism also became, then as now, the pejorative epithet that was attributed to any criticisms and suggestions for economic and social change their opponents wanted to stop).

They weren’t just critical ideas and lofty plans. The utopian socialists and their followers also sought to go beyond writing books and giving speeches by creating communities based on those ideas. This was particularly true in the United States, where more than 30 Fourierist phalanxes were established in the 1840s (two of the most famous being Brook Farm, in Massachusetts, and the Wisconsin Phalanx, in Ceresco). Owen himself financed and founded the community of New Harmony, in Indiana, based on his principles (where the Working Men’s Institute, Indiana’s oldest continuously operating public library, still exists).***

Eventually, as we will see in a later chapter, Marx and Engels developed a critique of the ideas put forward by the utopian socialists. But they also expressed a great deal of admiration for these initial socialist thinkers, and were certainly influenced by them during their steps toward the development of a critique of both mainstream economic theory and capitalism.

———

*To be clear, Saint-Simon’s definition of the working-class was not restricted to the contemporary meaning (according to which it consists of blue-collar workers or those without a college education), much less the Marxist notion (which will analyzed in detail in a later chapter), but included all people he considered to be engaged in productive work that contributed to society, such as industrialists, managers, scientists, and bankers, along with manual and skilled laborers.

**Fourier also criticized the repressive family structure, in which men treated their spouses as if they owned them and worked only for them and children had little freedom to express their deepest sentiments. He believed that humans should create more equitable relationships between the sexes and that equality could exist only if people were freed from the constraints of marriage. He thus advocated free love and the collective raising of children within the community.

***Hundreds of other “intentional communities,” many of them short-lived, proliferated during this time, especially in the United States (but also as far flung as Australia, where Herrnhut was founded in 1855). Only some of them were directly inspired by utopian socialism. The others often looked to religious leaders and principles of community for inspiration. In fact, the longest-lasting experiment with communism in the modern age was not as is generally presumed the Soviet Union (which lasted from 1922 to 1991), but the Shakers (from its first settlement at Watervliet, New York in 1774 to when the leaders of the United Society of Believers in Canterbury Shaker Village voted to close the Shaker Covenant in 1957).