Both the number of initial unemployment claims for unemployment compensation and the number of continued claims for unemployment compensation are once again on the rise, signaling a worsening of the Pandemic Depression.

This morning, the U.S. Department of Labor (pdf) reported that, during the week ending last Saturday, another 935 thousand American workers filed initial claims for unemployment compensation. While initial unemployment claims remain well below the peak of about seven million in March, they are far higher than pre-pandemic levels of about 200 thousand claims a week.

The number of continued claims for unemployment compensation, while also below its peak, rose from the previous week and was more than 20.6 million American workers—a figure that includes workers receiving Pandemic Unemployment Assistance.* This means that, since the end of April, the number of continued claims has fallen below 20 million only once (and that to 19 million, toward the end of November).

To put this number into further perspective, consider the fact that the highest number of continued claims for unemployment compensation during the Second Great Depression was 6.6 million (at the end of May 2009), and in the week before the Pandemic Depression began there were only 1.6 million continued claims by American workers.

In the meantime, at least 1,074 new coronavirus deaths and 40,607 new cases were reported in the United States yesterday. As of this morning, more than 6.1 million Americans have been infected with the coronavirus and at least 185.6 thousand have died—more than any other country in the world, which has received barely a mention from anyone in the Trump administration.

According to Gregory Daco, chief U.S. economist at Oxford Economics, “We are not moving in the right direction. With the looming expiration of benefits, it’s even more worrisome.”

In the meantime, at least 3,611 new coronavirus deaths and 245,033 new cases were reported in the United States yesterday—two morbid new records. As of this morning, more than 17 million Americans have been infected with the coronavirus and at least 307,642 have died. That’s more than any other country in the world, a crisis continues to receive barely a mention from anyone in the Trump administration.**

The result will be new waves of business slowdowns and closures, which in turn will mean millions more U.S. workers furloughed and laid off. Widespread inoculations of the U.S. and world populations are still many months off. Therefore, in the absence of a radical change in economic policies and institutions, Americans can expect to see steady streams of both initial unemployment claims and continued claims in the weeks and months ahead.

———

*This is the special program for business owners, the self-employed, independent contractors, and gig workers not receiving other unemployment insurance.

**The last time I posted a chart of unemployment claims, in early September, some 6.1 million Americans had been infected with the coronavirus and 185.6 thousand had died.

U.S. billionaires have recouped all of their wealth—and more—during the Pandemic Depression. Meanwhile, since May, the number of poor Americans has grown by about 8 million. And the number of American workers applying for and receiving unemployment benefits continues at record levels.

Pandemic be damned: America’s 400 richest are worth a record $3.2 trillion, up $240 billion from a year ago, aided by a stock market that has defied the virus.

When the Covid-19 pandemic began to sweep the world earlier this year, the wealth of U.S. billionaires plummeted in lockstep with the stock market. Yet, just six months after the market bottomed out—with hundreds of thousands Americans dead and the coronavirus still to be contained—the wealthiest Americans are doing better than ever. In other words, the pain, at least for the ultra-rich, was remarkably short lived.

Meanwhile, more and more American workers, who have lost their jobs or been furloughed, are attempting to survive on meager unemployment benefits. And many of them and their families—especially Black people and children—are now falling below the poverty line.

Part of the reason for this obscene growth in poverty is the expiration of the CARES Act’s $600 per week unemployment supplement. The other reason is that the number of American workers who are applying for unemployment benefits continues at elevated levels.

This morning, the U.S. Department of Labor (pdf) reported that, during the week ending last Saturday, another 898 thousand American workers filed initial claims for unemployment compensation. While initial unemployment claims remain well below the peak of about seven million in March, they are far higher than pre-pandemic levels of about 200 thousand claims a week.

The number of continued claims for unemployment compensation, while also below its peak, was still more than 25 million workers—a figure that includes workers receiving Pandemic Unemployment Assistance.*

To put this number in perspective, consider the fact that the highest number of continued claims for unemployment compensation during the Second Great Depression was 6.6 million (at the end of May 2009), and in the week before the Pandemic Depression began there were only 1.6 million continued claims.

In the meantime, at least 1,011 new coronavirus deaths and 59,751 new cases were reported in the United States yesterday. As of this afternoon, more than 7.9 million Americans have been infected with the coronavirus and at least 217.1 thousand have died—more than any other country in the world, grotesque outcomes that continue to receive barely a mention from Trump or anyone (aside from Dr. Anthony Fauci) in his administration.

Meanwhile, many colleges and universities that have attempted to reopen with students in residence are reporting hundreds of (and, in some cases, more than a thousand) novel coronavirus infections.

The result will be new waves of business slowdowns and closures, which in turn will mean millions more U.S. workers furloughed and laid off. Unless there is a radical change in economic policies and institutions, Americans can expect to see steady streams of new COVID-19 infections and deaths, initial and continued unemployment claims, and growing poverty in the weeks and months ahead.

As for those at the top: during the first six months of the pandemic, the United States added more than 29 more billionaires, increasing from 614 to 643. The Pandemic Depression has been a boon to their fortunes.

———

*This is the special program for business owners, the self-employed, independent contractors, and gig workers not receiving other unemployment insurance.

Year 3 of the Trump presidency was absolutely terrific—indeed, record-breaking—for Americans.

At least that’s how things look in terms of the headline numbers from the Census Bureau: median household income was up (by 6.8 percent, a record) over 2018 and the official poverty rate decreased (by 1.3 percentage points, to 10.5 percent, the lowest rate observed since estimates were initially published for 1959).*

And then there’s Kevin Hassett, former chair of Trump’s White House Council of Economic Advisers (who returned to the White House to lead its pandemic-response team, downplaying the danger of coronavirus and pushing the administration to re-open the economy amid lockdowns and social distancing) who seized on the report to make another of his wild claims:

If you’re a social justice warrior and you’re looking at the data, you would have to say that the Trump years, through the beginning of the pandemic, were the sort-of best years for advances in social justice since World War II.

The problem is that other data in the same report show nothing of the sort.

The distribution of income in the United States was just as grotesquely unequal in 2019 as it was in 2018 (and in every year both before and now during the Trump presidency). The highest quintile of American households captured 51.9 percent of income in the United States (it was 52 percent in 2018), the fourth quintile 22.7 percent (compared to 22.6 percent the previous year), and so on down the line. The lowest quintile got 3.1 percent, exactly the same as in 2018.

So no, no “social justice warrior” would be able to say the Trump years were the “best years for advances in social justice since World War II.”

In fact, quite the opposite. The economic policies of the Trump administration are both the product of and serving to reinforce the fundamental inequalities that have characterized the United States for decades now.

They’re also the reason why the novel coronavirus pandemic has hit the United States so savagely and unevenly. As I argued back in May, and Nick Hanauer and David M. Rolf recently concurred in Time,

Like many of the virus’s hardest hit victims, the United States went into the COVID-19 pandemic wracked by preexisting conditions. A fraying public health infrastructure, inadequate medical supplies, an employer-based health insurance system perversely unsuited to the moment—these and other afflictions are surely contributing to the death toll. But in addressing the causes and consequences of this pandemic—and its cruelly uneven impact—the elephant in the room is extreme income inequality.

The basis of their claim about inequality in the United States is a new working paper by Carter C. Price and Kathryn Edwards [ht: mfa] of the RAND Corporation, “Trends in Income From 1975 to 2018.”

While their general claim is pretty familiar (the pattern of capitalist growth in the United States during the two or three decades after World War II lowered the degree of inequality but, beginning in the mid-1970s, the trend was reversed and inequality rose during every decade), their analysis of the new pattern of capitalist growth reveals just how obscene it has been.

Consider the following conclusions from their study:

On average, extreme inequality is costing the median income full-time worker about $42,000 a year. Half of all full-time workers now earn less than half what they would have had incomes across the distribution continued to keep pace with economic growth.

The median male worker needed 30 weeks of income in 1985 to pay for housing, healthcare, transportation, and education for his family. By 2018, that “Cost of Thriving Index” had increased to 53 weeks (more weeks than in an actual year).

Two-income families are now working twice the hours to maintain a shrinking share of the pie, while struggling to pay housing, healthcare, education, childcare, and transportation costs that have grown at two to three times the rate of inflation.

Basically, according to Price and Edwards’s calculations, the income growth for most groups of Americans—thus, the bottom 25 percent, the median, the bottom 90 percent, and so on—was less than the rate of growth of real per capita Gross Domestic Product. Only the incomes of those in the top 5 percent grew at a faster rate. Thus, for example, the aggregate income for the population below the 90th percentile after 1975 would have been 67 percent higher in 2018 had income growth followed the pattern of the first two post-War decades.

The cumulative result over the past 45 years is that the members of the bottom 90 percent lost almost $50 trillion ($47 trillion or $48.6, depending on the price deflator used), which was seized by those at the top, especially the richest 1 percent of Americans.**

That pattern of unequal growth, which was inherited by the Trump administration, has simply not changed in the last three and a half years, no matter what Trump, Haslett, or the other “hacks and grifters” in the White House say.

Moreover, the monstrous inequalities that existed at the end of 2019 have shaped in profound ways both the effects of the spread of the coronavirus across the country and the early stages of the recovery from the Pandemic Depression. American economic economic and political elites have demanded and been able to implement policies that have only served to reinforce the unequalizing pattern of economic growth, which left most Americans vulnerable to the pandemic and to the resulting economic downturn.

The unequal pattern of capitalist growth in the United States documented in the new RAND report is exactly the opposite of what social justice warriors have been fighting for. Everyone, except the tiny group at the top, have been the ultimate losers.

———

*But there is a caveat on the median household income figures: the bureau’s main household survey for the report on Income and Poverty in the United States: 2019 was conducted in March and April of this year, as the pandemic was surging. That lowered the response rate, especially among low-income Americans. Still, the bureau estimates that median income in 2019 was about 4.1 percent higher than in 2018.

**The missing piece in the story told by Price and Edwards has to do with the mechanism of the massive transfer from the bottom 90 percent to those at the top. I have tried to fill in that missing piece, most recently in 2019 (e.g., here and here).

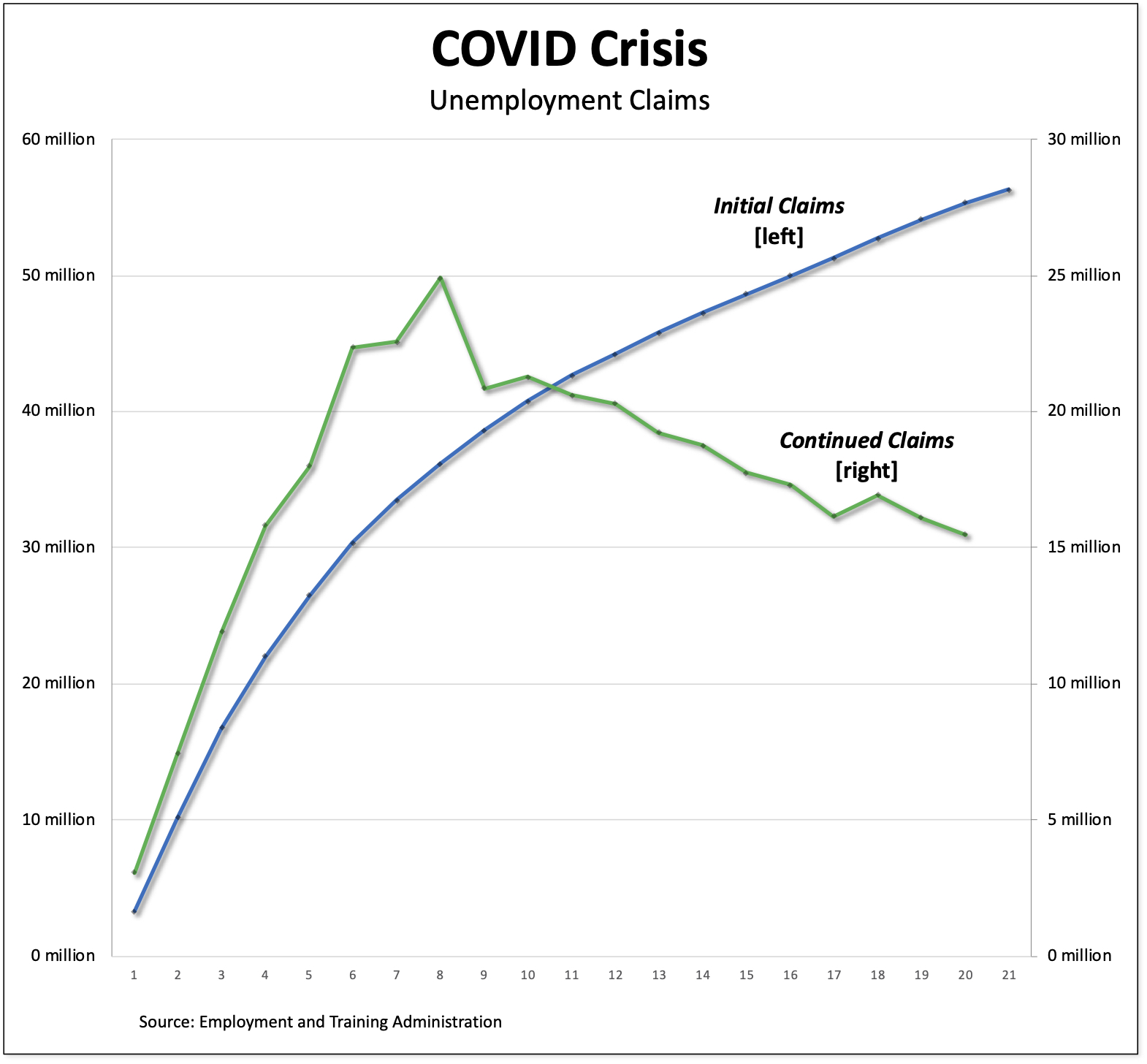

The number of initial unemployment claims for unemployment compensation in the United States fell below one million for only the second time since the beginning of the COVID crisis. But the number of continued claims for unemployment compensation is once again on the rise, signaling a continuation of the Pandemic Depression.

This morning, the U.S. Department of Labor (pdf) reported that, during the week ending last Saturday, another 881 thousand American workers filed initial claims for unemployment compensation. While initial unemployment claims remain well below the recent peak of about seven million in March, they are far higher than pre-pandemic levels of about 200 thousand claims a week.

The number of continued claims for unemployment compensation, while below its peak, rose from the previous week and was more than 29 million American workers—a figure that includes workers receiving Pandemic Unemployment Assistance.*

To put this number in perspective, consider the fact that the highest number of continued claims for unemployment compensation during the Second Great Depression was 6.6 million (at the end of May 2009), and in the week before the Pandemic Depression began there were only 1.6 million continued claims.

In the meantime, at least 1,074 new coronavirus deaths and 40,607 new cases were reported in the United States yesterday. As of this morning, more than 6.1 million Americans have been infected with the coronavirus and at least 185.6 thousand have died—more than any other country in the world, which has received barely a mention from anyone in the Trump administration.

Meanwhile, many colleges and universities that have attempted to reopen with students in residence are reporting hundreds of (and, in some cases, more than a thousand) novel coronavirus infections.

The result will be new waves of business slowdowns and closures and schools returning to online teaching, which in turn will mean millions more U.S. workers furloughed and laid off. Unless there is a radical change in economic policies and institutions, Americans can expect to see steady streams of both initial unemployment claims and continued claims in the weeks and months ahead.

———

*This is the special program for business owners, the self-employed, independent contractors, and gig workers not receiving other unemployment insurance.

Right now, the United States is mired in an economic depression, the Pandemic Depression, not dissimilar to what happened in the 1930s and again after the crash of 2007-08.

Real (inflation-adjusted) gross domestic product contracted by an annual rate of 31.7 percent in the second quarter of 2020 (according to the Bureau of Economic Analysis) and at least 27 million American workers are currently unemployed (counting workers continuing to receive some kind of unemployment benefits, according to my own calculations).* By all accounts—from both macroeconomic data and anecdotes reported in the media—the current situation is an economic and social disaster equivalent to what the United States went through during the first and second Great Depressions.

The question is, does mainstream macroeconomics have anything to offer in terms of insights about the causes of the current crises or what should be done to solve them?

Many readers are, I’m sure, skeptical, given the abysmal track record of mainstream macroeconomic thinking in the United States. Going back just a bit more than a decade, to the Second Great Depression, it’s clear that mainstream macroeconomists failed on all counts: they didn’t predict the crash; they didn’t even include the possibility of such a crash within their basic theory or models; and they certainly didn’t know what to do once the crash occurred.

Can they do any better with the current depression?

The example I want to use was recently posted by Harvard’s Greg Mankiw, the author of the best-selling macroeconomics textbook on the market. I know it’s not the most sophisticated (or, if you prefer, technical or detailed) discussion out there but it does matter: next year, thousands upon thousands of students will receive their basic training in mainstream macroeconomic theory and its application to the Pandemic Depression from Mankiw’s text.

It should come as no surprise that Mankiw uses the macroeconomic model—of aggregate demand and supply—he has so laboriously built up over the course of many chapters to examine what he calls “the economic downturn of 2020.” His basic argument is that, first, aggregate demand declined (shifting to the left, from AD1 to AD2) due to a decline in the velocity of money (one of the exogenous variables that, in mainstream moderls, determines aggregate demand), and second, the long-run aggregate supply curve declines (shifts left, from LRAS1 to LRAS2), while the short-run aggregate supply curve (SRAS) stays the same. The result is a decline in output (the left-facing arrow at the bottom of the diagram).

This is all pretty straightforward stuff. Except: Mankiw wants to argue that it’s the “natural level of output” as represented by the long-run aggregate supply curve, not the perfectly elastic (or horizontal) short-run aggregate supply curve, that shifts to the left. Huh?

His only explanation is that

When a pandemic strikes and many businesses are temporarily closed, aggregate demand falls because people are staying at home rather than spending at those businesses. Because those businesses cannot produce goods and services, the economy’s potential output, as reflected in the LRAS curve, falls as well. The economy moves from point A to point B.

The problem is, there’s nothing in the way Mankiw has derived the long-run aggregate supply curve—from given resources (land, labor, and capital) and technology—that has changed. Instead, the shutdown of many businesses merely means that there’s enormous excess capacity in the economy. The “natural rate of output”—the level of output corresponding to the “natural level of unemployment”—remains as it was.

But Mankiw is trapped by his own model. The benefit of analyzing the current depression in terms of a shift in the long-run aggregate supply curve is that, as soon as the shutdown is lifted, the supply curve shifts back to the right and the economy moves back to its old long-run equilibrium. Problem solved!

And if the long-run aggregate supply curve doesn’t shift back to the right? Well, then, U.S. capitalism has in fact destroyed its resources—especially labor power—and the economy doesn’t recover, at least anytime soon.

Moreover, if he’d shifted the short-run aggregate supply curve (up in the diagram), well, then we’re in the land of inflation—with the price level rising—an even more severe decline in economic activity (smaller than B), and no return to long-run equilibrium. But prices are not, in general rising, which is why he uses the horizontal short-run aggregate supply curve in the first place (to reflect fixed prices, the result of monopoly enterprises).

Not only is Mankiw trapped by the logic of his own model. His analysis—both the model and the accompanying text—leaves out much of what is interesting and important about the Pandemic Depression.

We’ve seen, for example, that U.S. stock markets, after an initial downturn, have soared to new record highs, even as national output declines and unemployment reached numbers of workers not seen since the Great Depression of the 1930s. That doesn’t even warrant a mention in Mankiw’s analysis—which involves a discussion of assistance to workers and small businesses but nothing about the trillions of dollars available to the Treasury and Federal Reserve to bailout large corporations, keep credit flowing, and boost equity markets.

But there’s an even larger problem in Mankiw’s basic model: all downturns, whether recession or depressions, are the result of “accidents.”

Some surprise event shifts aggregate supply or aggregate demand, reducing production and employment. Policymakers are eager to return the economy to normal levels of production and employment as quickly as possible.

And the Pandemic Depression? Well, according to Mankiw, it was “by design.” But the distinction is meaningless: in all cases, the downturn occurs because of something outside the model—by some kind of “shock.”

So, capitalism itself is absolved. In Mankiw’s model, and in mainstream macroeconomics more generally, there’s nothing in capitalism itself—how profit rates behave, what decisions capitalists make, the fragility of the financial sector, obscene levels of inequality, and so on—that causes the economy to collapse.

If we step outside the confines of Mankiw’s model, then we can begin to see how U.S. capitalism, while it did not create the novel coronavirus, certainly produced and exacerbated the destructive effects of the pandemic on the American economy. For example, after decades of neglect of the public healthcare system and attempts to shore up the private provision of healthcare in the United States, the country was ill-prepared to diagnosis and contain the pandemic. Even more, it worsened the already-grotesque inequalities of healthcare—as well as incomes, wealth, and household finances—it had originally created.

That same economic system also left in the hands of private employers—not the government or workers themselves—the decisions of whether to keep workers employed or, as happened across the country, to furlough or lay off tens of millions of their employees. Any to add to the misery: many of the workers who were supposed to be on temporary layoffs are now finding they’ve lost their jobs permanently and are spending more and more time attempting to find new jobs.

None of those pre-existing economic conditions figures in Mankiw’s analysis. They can’t, because they don’t exist within mainstream macroeconomics, which has been studiously constructed precisely to provide a hydraulic model of macroeconomic equilibrium—starting with full employment and price stability, one or another external “shock” that moves the economy away from there, and then automatic mechanisms to return the economy to its original position—on the basis of aggregate demand and aggregate supply.

And that’s how we get Mankiw’s excuse for the Pandemic Depression:

given the circumstances, a large economic downturn was arguably the best outcome that could be achieved.

———

*Millions more workers are either unemployed but not receiving benefits or involuntarily underemployed, working part-time (often with cuts in pay and benefits) when they prefer to be working full-time.

The number of initial claims for unemployment compensation in the United States once again surpassed one million—for the 21st time in the past 22 weeks—signaling a continuation of the Pandemic Depression.

This morning, the U.S. Department of Labor (pdf) reported that, during the week ending last Saturday, another 1 million American workers filed initial claims for unemployment compensation. While initial unemployment claims remain well below the recent peak of about seven million in March, they are far higher than pre-pandemic levels of about 200 thousand claims a week.

The number of continued claims for unemployment compensation has also fallen from its peak but the total from the previous week (the series of continued claims lags initial claims by one week) was still 27 million American workers—a figure that includes workers receiving Pandemic Unemployment Assistance.*

To put this number in perspective, consider the fact that the highest number of continued claims for unemployment compensation during the Second Great Depression was 6.6 million (at the end of May 2009), and in the week before the Pandemic Depression began there were only 1.6 million continued claims.

In the meantime, at least 1,193 new coronavirus deaths and 44,934 new cases were reported in the United States yesterday. As of this morning, more than 5.9 million Americans have been infected with the coronavirus and at least 179.9 thousand have died—more than any other country in the world, which has received barely a mention during the Republican national convention.

The result will be new waves of business slowdowns and closures, which in turn will mean millions more U.S. workers furloughed and laid off. Unless there is a radical change in economic policies and institutions, Americans can expect to see steady streams of both initial unemployment claims and continued claims in the weeks and months ahead.

———

*This is the special program for business owners, the self-employed, independent contractors, and gig workers not receiving other unemployment insurance.

The number of initial unemployment claims for unemployment compensation in the United States once again increased, to over one million. But the cumulative number of initial claims is still staggering, reaching 57.4 million workers by the end of last week.

This morning, the U.S. Department of Labor (pdf) reported that, during the week ending last Saturday, another 1.1 million American workers filed initial claims for unemployment compensation. They’re the third group to file for unemployment claims during the pandemic who are not going to benefit from the additional $600 benefit that was authorized in the CARES Act but which has now expired. Moreover, funds from the Paycheck Protection Program, which gave grants and loans to companies to keep workers on payroll, have been running out for many recipients.

I can’t pay my rent, electric bill, food, or car payments. I’m able to get the bare minimum with my allotted food stamps

said Sabrina Wickward Arce, a cosmetologist who is struggling to find a new job in Miami, Florida.

Here is a breakdown of each of the past twenty-two weeks:

• week ending on 21 March—3.31 million

• week ending on 28 March—6.87 million

• week ending on 4 April—6.62 million

• week ending on 11 April—5.24 million

• week ending on 18 April—4.44 million

• week ending on 25 April—3.87 million

• week ending on 2 May—3.18 million

• week ending on 9 May—2.69 million

• week ending on 16 May—2.45 million

• week ending on 23 May—2.12 million

• week ending on 30 May—1.90 million

• week ending on 6 June—1.57 million

• week ending on 13 June—1.54 million

• week ending on 20 June—1.48 million

• week ending on 27 June—1.41 million

• week ending on 4 July—1.31 million

• week ending on 11 July—1.31 million

• week ending on 18 July—1.42 million

• week ending on 25 July—1.44 million

• week ending on 1 August—1.19 million

• week ending on 8 August—971 thousand

• week ending on 8 August—1.11 million

While the number of continued claims for unemployment compensation has continued to fall from its peak, the total from the previous week (the series of continued claims lags initial claims by one week) was still 14.8 million workers. And we need to add to that an additional 11.2 million workers receiving Pandemic Unemployment Assistance.* Therefore, approximately 26 million workers are jobless and receiving some form of unemployment compensation.

To put this number in perspective, consider the fact that the highest number of continued claims for unemployment compensation during the Second Great Depression was 6.6 million (at the end of May 2009), and in the week before the COVID Crisis there were only 1.8 million continued claims.

In the meantime, at least 1,295 new coronavirus deaths and 43,006 new cases were reported in the United States yesterday. As of this morning, more than 5.5 million Americans have been infected with the coronavirus and at least 173 thousand have died—with no end in sight.

The United States can therefore expect to experience new waves of business closures, which in turn will mean more American workers furloughed and laid off, and therefore steady streams of both initial unemployment claims and continued claims, in the weeks and months ahead.

———

*This is the special program for business owners, the self-employed, independent contractors, and gig workers not receiving other unemployment insurance.

The number of initial unemployment claims for unemployment compensation in the United States fell below one million for the first time since the beginning of the COVID crisis. But the cumulative number of initial claims is still staggering, reaching 56.3 million workers by the end of last week.

This morning, the U.S. Department of Labor (pdf) reported that, during the week ending last Saturday, another 963 thousand American workers filed initial claims for unemployment compensation. They’re the second group to file for unemployment claims during the pandemic who are not going to rise the additional $600 benefit that was authorized in the CARES Act.

Here is a breakdown of each of the past twenty-one weeks:

• week ending on 21 March—3.31 million

• week ending on 28 March—6.87 million

• week ending on 4 April—6.62 million

• week ending on 11 April—5.24 million

• week ending on 18 April—4.44 million

• week ending on 25 April—3.87 million

• week ending on 2 May—3.18 million

• week ending on 9 May—2.69 million

• week ending on 16 May—2.45 million

• week ending on 23 May—2.12 million

• week ending on 30 May—1.90 million

• week ending on 6 June—1.57 million

• week ending on 13 June—1.54 million

• week ending on 20 June—1.48 million

• week ending on 27 June—1.41 million

• week ending on 4 July—1.31 million

• week ending on 11 July—1.31 million

• week ending on 18 July—1.42 million

• week ending on 25 July—1.44 million

• week ending on 1 August—1.19 million

• week ending on 8 August—0.96 million

While the number of continued claims for unemployment compensation has continued to fall from its peak, the total from the previous week (the series of continued claims lags initial claims by one week) was still 15.5 million workers. And we need to add to that an additional 10.7 million workers receiving Pandemic Unemployment Assistance.* Therefore, as of 10 days ago, 26.2 million workers were receiving some form of unemployment compensation.

To understand the magnitude of this figure, we need to compare it to the number of continued claims in late May 2009 (6.6 million), the worst point of the so-called Great Recession. Right now, in the midst of the Pandemic Depression, the number of American workers receiving unemployment compensation is 4 times what it was at the nadir of the Second Great Depression.

In the meantime, at least 1,478 new coronavirus deaths and 54,187 new cases were reported in the United States on 12 August. As of this afternoon, more than 5,217,000 Americans have been infected with the coronavirus and at least 166,100 have died. The three-day rolling average of new cases per million people in the country was 153.4 compared to 32.5 cases for the world as a whole.

We can therefore expect to see new waves of business closures, which in turn will mean more American workers furloughed and laid off, and therefore steady streams of both initial unemployment claims and continued claims, in the weeks and months ahead.

*This is the special program for business owners, the self-employed, independent contractors, or gig workers not receiving other unemployment insurance.

Mainstream economists and commentators, it seems, are worried that the global economy is going to come crashing down as a result of the COVID crisis. That’s why they’re willing now to consider the possibility that the current crisis is more than a normal recession, more serious even than the so-called Great Recession; in their view, it’s an economic depression.

That, at least, is the argument they present up front. But there’s something else going on, which haunts their analysis—that capitalism itself is now being called into question.

But before we get to that alarming specter, let’s take a look at the logic of their analysis about the current perils to the global economy—starting with the Washington Post columnist Robert J. Samuelson, who is basically taking his cues from a recent essay in Foreign Affairs by Carmen Reinhart and Vincent Reinhart.*

Their shared view is that the current slowdown is both more severe and more widespread than the crash of 2007-08, and the recovery will be much slower. Therefore, they argue, the COVID crisis represents the worst economic downturn since the Great Depression of the 1930s.

This is a big deal: mainstream economists and commentators are uneasy about invoking the term “economic depression.” They certainly resisted it for the crisis that occurred just over a decade ago, eventually devising a Goldilocks nomenclature, dubbing it the Great Recession (not as hot as the Great Depression but not as cold as a normal recession). As regular readers know, I had no compunction about calling it the Second Great Depression. And, according to their own logic, neither Samuelson nor the Reinharts should have either.

According to Barry Eichengreen and Kevin O’Rourke, the financial crisis and recession had led to as big a downward shock to global industrial production in 2008 as the 1929 financial crisis, and had pounded stock market values and world trade volumes harder in 2008-09 than in 1929-30. Thus, from the perspective of the magnitude of the initial shock, the global economy was in at least as dire shape after the crash of 2008 as it had been after the crash of 1929.

Moreover, the downturn that began in 2007-08 was “largely a banking crisis” (as the Reinharts put it) only if they ignore the grotesque levels of inequality that preceded the crash (based on stagnant wages and rising profits)—which in turn fueled the need for credit on the part of workers and the growth of the finance sector that both recycled corporate profits to workers in the form of loans and led to even higher profits, creating in the process a veritable house of cards. At some point, it would all come crashing down. And, eventually, it did.

In any case, Samuelson and the Reinharts are now willing to take the next step and use the dreaded d-word to characterize current events. Here’s how the Reinharts see things:

In its most recent analysis, the World Bank predicted that the global economy will shrink by 5.2 percent in 2020. The U.S. Bureau of Labor Statistics recently posted the worst monthly unemployment figures in the 72 years for which the agency has data on record. Most analyses project that the U.S. unemployment rate will remain near the double-digit mark through the middle of next year. And the Bank of England has warned that this year the United Kingdom will face its steepest decline in output since 1706. This situation is so dire that it deserves to be called a “depression”—a pandemic depression.

And Samuelson does them one better:

In one respect, the Reinharts have underestimated the parallels between the today’s depression and its 1930s predecessor. What was unnerving about the Great Depression is that its causes were not understood at the time. People feared what they could not explain. The consensus belief was that business downturns were self-correcting. Surplus inventories would be sold; inefficient firms would fail; wages would drop. The survivors of this brutal process would then be in a position to expand.

Something similar is occurring today.

Clearly, Samuelson and even more the Reinharts are worried that the global economy—their cherished vision of the free movement of capital (but not people) and expanding trade according to comparative advantage—is currently being imperiled and may not recover for years to come. The volume of world trade is down; the prices of many exports have fallen; corporate debt is climbing; and the reserve army of unemployed and underemployed workers is massive and still growing. The prospects for a return to business as usual are indeed remote.

That’s pretty straightforward stuff, and anyone who’s looking at the numbers can’t but agree. What we’re witnessing is in fact a Pandemic—or, in my view, a Third Great—Depression.

But that’s when things start to get interesting. Because the Reinharts do understand (although I doubt Samuelson does, since he’s really only concerned about government deficits) that, when you resurrect the term depression and invoke the analogy of the 1930s, you also call forth widespread discontent, massive protest movements, and challenges to capitalism itself. Here’s how they see it:

The economic consequences are straightforward. As future income decreases, debt burdens become more onerous. The social consequences are harder to predict. A market economy involves a bargain among its citizens: resources will be put to their most efficient use to make the economic pie as large as possible and to increase the chance that it grows over time. When circumstances change as a result of technological advances or the opening of international trade routes, resources shift, creating winners and losers. As long as the pie is expanding rapidly, the losers can take comfort in the fact that the absolute size of their slice is still growing. For example, real GDP growth of four percent per year, the norm among advanced economies late last century, implies a doubling of output in 18 years. If growth is one percent, the level that prevailed in the shadow of the 2008–9 recession, the time it takes to double output stretches to 72 years. With the current costs evident and the benefits receding into a more distant horizon, people may begin to rethink the market bargain.

Now, it’s true, their stated fear is that “populist nationalism” will disrupt multilateralism, open economic borders, and the free flow of capital and goods and services across national boundaries. That’s as far as their stated thinking can go.

But the apparition that lurks in the background is that rethinking the “market bargain”—what elsewhere I have called the “pact with the devil,” that is, giving control of the surplus to the top 1 percent as long as they made decisions to create jobs, fund schools and healthcare, and be able to tackle problems like the novel coronavirus pandemic so that the majority of people could lead decent lives—will mean expanding criticisms of capitalism and the search for radical alternatives.

That’s the real specter that haunts the Pandemic Depression.

*Samuelson sees the wife-and-husband Reinharts as “heavy hitters” among economists: “She is a Harvard professor, on leave and serving as the chief economist of the World Bank; he was a top official at the Federal Reserve and is now chief economist at BNY Mellon.”