Posts Tagged ‘war’

Cartoons of the day

Posted: 3 October 2020 in UncategorizedTags: Biden, cartoons, election, healthcare, police, taxes, Trump, violence, war

0

Cartoons of the day

Posted: 17 September 2020 in UncategorizedTags: Bush, cartoons, health, healthcare, hunger, Left, Obama, OWS, rent, Trump, unemployed, war

Cartoon of the day

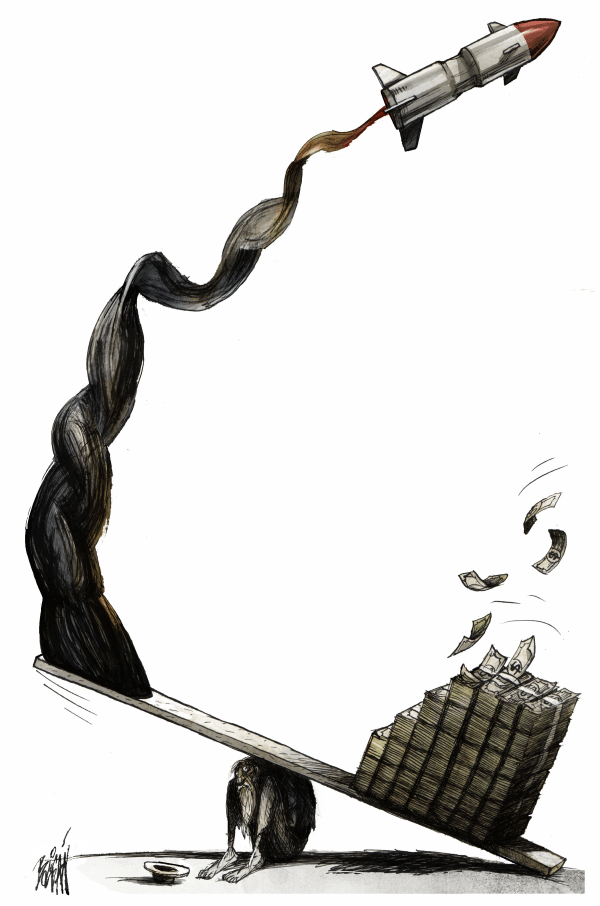

Posted: 15 July 2020 in UncategorizedTags: bailout, capitalism, cartoon, coronavirus, deaths, democracy, environment, healthcare, justice, pandemic, peace, schools, war

Special mention

Cartoon of the day

Posted: 1 May 2020 in UncategorizedTags: cartoon, coronavirus, education, health insurance, meat, nationalism, pandemic, rich, student debt, tax cuts, trickledown, Trump, United States, war, workers

Special mention

Cartoon of the day

Posted: 20 February 2020 in UncategorizedTags: Bloomberg, capitalism, capitalists, cartoon, Trump, United States, war

Special mention

Cartoon of the day

Posted: 4 February 2020 in UncategorizedTags: art, Bernie Sanders, cartoon, Democrats, impeachment, Mitch McConnell, MOMA, philanthropy, profits, Senate, Trump, war

Special mention

Cartoon of the day

Posted: 1 February 2020 in UncategorizedTags: Boris Johnson, Brexit, cartoon, EPA, GOP, ICE, immigration, impeachment, Iraq, Republicans, Trump, United Kingdom, United States, war

Special mention

Cartoon of the day

Posted: 1 February 2020 in UncategorizedTags: Boris Johnson, Brexit, cartoon, EPA, GOP, ICE, immigration, impeachment, Iraq, Republicans, Trump, United Kingdom, United States, war

Special mention

Cartoon of the day

Posted: 17 January 2020 in UncategorizedTags: cartoon, disaster, earthquake, GOP, healthcare, military, poverty, Puerto Rico, Republicans, Trump, United States, war

Special mention

Cartoon of the day

Posted: 16 January 2020 in UncategorizedTags: Boeing, cartoon, CEO, impeachment, New Year, student debt, Trump, war

Special mention