Everyone knows that inflation in the United States is increasing. Anyone who has read the news, or for that matter has gone shopping lately. Prices are rising at the fastest rate in decades. The Consumer Price Index rose 8.6 percent in March, which is the highest rate of increase since December 1981 (when it was 8.9 percent).

Clearly, inflation is hurting lots of people—especially the elderly living on fixed incomes and workers whose wages aren’t keeping up the price increases. No mystery there.

The only real mystery is, what’s causing the current inflation? That’s where things gets interesting.

To listen to or read mainstream economists the answer to the whodunnit is workers’ wages. They’re going up too fast, because the level of unemployment is too low and their employers are forced to pay them higher wages. As a result, corporations are compelled to raise their prices. Therefore, something has to be done (like increasing interest rates) to slow down the economy and force more workers into the Reserve Army of the Underemployed and Unemployed.*

The U.S. economy still looks overheated. Rising wages are a good thing, but right now they’re rising at an unsustainable pace. . .

This excess wage growth probably won’t recede until the demand for workers falls back into line with the available supply, which probably — I hate to say this — means that we need to see unemployment tick up at least a bit.

The amazing thing about Krugman’s story, and that of most mainstream economists, is there’s not a single word about profits. Corporate profits are entirely missing from their story. Inflation is only caused by workers’ wages, not the surplus raked in by U.S. corporations. Which is pretty amazing, given the numbers.

A quick look at the chart at the top of the post shows what’s been going on in the U.S. economy. Workers’ wages (the red line in the chart, the hourly wages of production and nonsupervisory workers) rose during 2021 at an annual average rate of less than 5 percent (ranging from 2.8 percent in the second quarter to 6.4 percent in the final quarter).

And profits? Well, they’ve been growing at astounding rates, magnitudes more than wages. Corporate profits (the light green line) rose during 2021 at an average rate of 40 percent, and the profits of nonfinancial corporations (the dark green line) expanded by even more: 69 percent!

Hmmm. . .

The fact that profits are entirely missing from the mainstream story about inflation reveals a fundamental problem within mainstream economic theories. On one hand, in their macroeconomics, wages and not profits are always the culprit. That’s because they only have a labor market, and not a capital market (much less a profit rate or, for that matter, a rate of surplus-value), when they analyze fluctuations in prices and output. It’s as if corporate profits are only a residual—what is left over in the difference between wages and wage-driven prices. On the other hand, in their microeconomics, profits represent the return to capital, and thus a key component of commodity prices as well as the driver of economic growth.

Such “capital fetishism” means that profits as the return to a thing, capital, play an important role in the mainstream theory of value but then disappear entirely in the macroeconomic story about inflation.

It’s therefore a problem in the basic theories of mainstream economics. And it’s a problem when it comes to their economic policies: anything and everything must be done to keep workers’ wages in check, and (without ever mentioning them) to safeguard corporate profits.

The fact is, once we solve the mystery of the missing profits we can actually tackle the problem of inflation. But neither mainstream economists nor the leaders of corporate America are going to like what we come up with.

___

*The Federal Reserve is suggesting that it can raise interest rates to get prices down “without causing a recession.” In fact, according to research from the investment bank Piper Sandler, the Fed raised rates to combat inflation nine different times during the past 60 years, and on eight of those occasions a recession occurred not long after.

In this post, I continue the draft of sections of my forthcoming book, “Marxian Economics: An Introduction.” The first five posts (here, here, here, here, and here) will serve as the basis for chapter 1, Marxian Economics Today. The text of this post is for Chapter 2, Marxian Economics Versus Mainstream Economics (following on from the previous posts, here, here, here, and here).

Limits of Mainstream Economics Today

Keynes’s criticisms of neoclassical economics set off a wide-ranging debate that came to define the terms of—and, ultimately, the limits of debate within—mainstream economics.

On one side are neoclassical economists, who celebrate the invisible hand and argue that markets are the best way to efficiently allocate scarce resources. On the other side are Keynesian economists, who argue instead for the visible hand of government intervention to move markets toward full employment.

That tension, between the theories and policies of neoclassical and Keynesian economics, is the reason why in most colleges and universities the principles of economics are taught in two separate courses: microeconomics and macroeconomics. Moreover, the tension between the two schools of thought plays out within every area of economics, including (but certainly not limited to) microeconomics and macroeconomics.

One way of understanding the differences between the two approaches is to think about them as conservative and liberal interpretations of mainstream economics. Conservative mainstream economics tend to presume that the basic assumptions of neoclassical economics hold in contemporary capitalism, while liberal mainstream economists think they don’t.

Let’s consider two examples. First, within microeconomics, conservative mainstream economists (such as the late Milton Friedman) believe that individuals make rational decisions within perfectly competitive markets. Therefore, if markets exist, they should be allowed to operate within any regulations; and, if a market doesn’t exist, it should be created. Liberal mainstream economics (such as Joseph Stiglitz), on the other hand, see both individual decisions and markets as being imperfect—because individuals have limited or asymmetric information, some firms have more market power than others, and so on. Therefore, they argue, markets need to be guided to the best outcome.

The second example is from macroeconomics. The view of conservative mainstream economists (such as Thomas J. Sargent) is that capitalism operates at or close to full employment (where, in the chart above, aggregate demand intersects the vertical portion of the aggregate supply curve), whereas liberal mainstream economists (such as Paul Krugman) believe that unregulated markets often lead to considerable unemployment (where aggregate demand intersects the horizontal portion of the aggregate supply curve, at level of output less than full employment).*

To attempt to reconcile the two competing views, many mainstream economists argue for a “middle position”—somewhere between the opposed neoclassical and Keynesian views. There (in the red portion of the aggregate supply curve), mainstream economists find a tradeoff between increases in output and changes in the price level, that is, between inflation and unemployment.

And the predominant view within mainstream economics shifts back and forth between the two poles. Sometimes, as in the years before the crash of 2007-08, mainstream economics moved closer to the neoclassical approach. That’s when policies such as deregulation, privatization, the reduction of government deficits, welfare reform, and so on were all the rage, within both academic and political circles. After the crash, when the neoclassical approach was said to have failed, mainstream economics swung back in other direction. That’s when there were calls for more government intervention and fewer worries about budget deficits and the like.

In the midst of the Pandemic Depression, much the same kind of debate between advocates of the two poles of mainstream economics has been taking place. On one side, conservative mainstream economists have argued in favor of rescuing banks and corporations, such that an economic recovery would “trickle down” to workers and their households. Liberal mainstream economists, on the other hand, have favored direct payments to workers who were furloughed or laid off—an idea that was attacked by their conservative counterparts, because such payments were seen as providing a “disincentive” for workers to return to their jobs.

Every time capitalism enters into crisis, the same kind of debate breaks out between conservative and liberal economists (and, of course, between different groups of politicians and voters).

If mainstream economists are so divided between the two approaches, what in the end unites them into what I have been calling mainstream economics? Like all such labels, it is defined in part by what it includes, and in part by what it excludes.

What mainstream economics includes is the idea that neoclassical and Keynesian approaches establish the limits within which theoretical and policy debates can and should take place. Together, they define what is in the “economic toolkit,” and therefore what it means to “think like an economist.” Moreover, the two groups of economists argue that capitalist markets are the way a modern economy can and should be organized. They may disagree about the relevant approach—for example, the “invisible hand” of free markets versus the “visible hand” of government intervention. But they all agree on the goal: to create the appropriate institutional environment so that capitalist markets work properly.

They also share the view that the only way capitalism operates falls below its general equilibrium, full-employment potential is because of some external “shock.” In other words, all economic downturns, such as recessions and depressions, are due to external causes, not because of anything internal to the normal workings of capitalism.

What the definition of mainstream economics excludes is any approach, such as Marxian economics, that is based on a theoretical approach that lies outside the protocols of neoclassical and Keynesian economics. So, for example, the idea of class exploitation is generally overlooked or ignored within mainstream economics. Similarly, imagining and creating ways of allocating resources other than through capitalist markets are pushed to or beyond the margins by mainstream economists.

Together, the inclusions and exclusions contained within the definition of mainstream economics serve to define what mainstream economists think and do in their theoretical practice as well as in the policy advice they offer.

———

*As many contemporary Post Keynesian economists have noted, when neoclassical and Keynesian were combined in a single approach to economics (for example, in the “neoclassical synthesis” in the decades following World War II), many of the critical aspects of Keynes’s writings—including the notion of uncertainty and the idea that much stock market investment was merely speculation and added little to the productive capacity of the “real” economy—were downplayed or ignored altogether.

In this post, I continue the draft of sections of my forthcoming book, “Marxian Economics: An Introduction.” This, like the previous two posts, is for chapter 1, Marxian Economics Today.

Beyond the Mainstream

This is certainly not the first time people have looked beyond mainstream economics. There is a long history of criticisms of both mainstream economic theory and capitalism from the very beginning. Although students won’t have read about them in traditional economics textbooks.

Those texts are generally written with the presumption there’s only one economic theory and one economic system. The existence of Marxian economics opens up the debate, creating space for both multiple ways of thinking about economics and a variety of different economic systems.

Criticisms of Mainstream Economic Theory

In the history of economic thought, criticisms of the mainstream approach were formulated early on. Adam Smith, David Ricardo, and others (such as Jean-Baptiste Say, Thomas Robert Malthus, and John Stuart Mill) developed classical political economy in the late-eighteenth and early-nineteenth centuries, when the new economic system we now call capitalism was just getting off the ground—and almost immediately their approach was debated and challenged.

The classical political economists developed a labor theory of value to analyze the value of commodities, the goods and services that were bought and sold on markets. They utilized that labor theory of value to then argue that capitalism, based on increasing productivity and free international trade, would lead to the growth of industry and an increase in the wealth of nations.

The early critics of classical political economy included a wide variety of writers, especially in the United Kingdom and Western Europe, from Thomas Carlyle (an English Romantic who expressed his opposition to the market system, because it rewarded “salesmanship” and not hard work) and John Barton (a British Quaker who argued that the introduction of labor-saving machinery would permanently displace workers who would not be absorbed by other branches of industry) to Jean-Charles-Léonard Simonde de Sismondi (a Swiss historian who viewed capitalism as being detrimental to the interests of the poor and particularly prone to crisis brought about by an insufficient general demand for goods) and Thomas Hodgskin (an English socialist, critic of capitalism, and defender of both free trade and early trade unions).

In the middle of the nineteenth century, Marx (along with his friend and frequent collaborator Friedrich Engels) became a close student of classical political economy, developing his now-famous critique. During the course of his writings, he expressed both admiration for and opposition to the methods and the conclusions of the classical political economists. Over the course of this book, we will examine in considerable detail the ways Marx and later Marxian economists both built on and broke from classical political economy.

But the debate about early mainstream economics didn’t stop there.

In the late 1800s, a new school of economic thought, neoclassical economics was created, which represented both an extension of and break from classical political economy, although in a manner quite different from that of Marx. The early neoclassicals—such as William Stanley Jevons, Karl Menger, and Léon Walras—rejected the classicals’ labor theory of value, in favor of consumer utility, but accepted the classicals’ celebration of capitalism’s rising productivity and free trade. Hence, both the “neo” and the “classical” of their name.

The neoclassical economists’ basic argument was that, if all markets are allowed to operate freely, all consumers would maximize utility, all firms would maximize profits, and the economy as a whole would reach full employment. The “invisible hand” became the central thesis of contemporary mainstream microeconomics.

And it had general validity within mainstream economics until the Great Depression of the 1930s, when in the United States and elsewhere capitalist economies crashed and the unemployment rate soared to over 25 percent. Not surprisingly, the neoclassical orthodoxy was challenged at the time by many economists, including John Maynard Keynes. Keynes’s idea was that, because of fundamental uncertainty, especially on the part of investors, it was highly likely that capitalist economies would regularly operate at less-than-full employment. The need for the “visible hand” of government intervention to achieve full employment was the basis of the mainstream macroeconomics.

Attempts to combine neoclassical microeconomics and Keynesian macroeconomics—the invisible hand of markets and the visible hand of government fiscal and monetary policy—have defined mainstream economics ever since. That’s why, today, in most departments, mainstream economics is still taught in two separate courses, microeconomics and macroeconomics. And very few of them include any references to other approaches, especially Marxian economics.

Criticisms of Capitalism

Just as mainstream economic theory has been challenged from the very beginning, so has capitalism, the economic and social system celebrated by mainstream economists.

Perhaps the most famous early mass movement against capitalism was directed by the Luddites, a radical faction of English textile workers who in the early-nineteenth century attacked mills and destroyed textile machinery as a form of protest against low pay and harsh working conditions. While the name has come to be associated with anyone opposed to the use of new technologies, the actual historical movement objected to machinery that was introduced to speed up production and change the terms of negotiation in favor of employers and against workers.

Later, when workers were able to form labor unions—against a great deal of opposition from their employers and governments that backed those employers—they developed new strategies to challenge the ways they were considered and treated within capitalism. They often demanded higher pay, more secure employment, additional benefits, and even a say in how the enterprises in which they worked were managed. Depending on the situation, they set up picket lines, went on strike, occupied their workplaces, and organized unemployed workers. In many cases, while the workers were primarily concerning with meeting their daily needs, their activities were treated as attacks on capitalism itself.

That was certainly the case in the campaign for an eight-hour workday, which reached its peak in May 1886 in Haymarket Square in Chicago. It began as a peaceful rally to limit the length of the workday (at the time, workers were regularly required to labor much longer—often 10, 12, or more hours a day, without overtime pay) and then, when the police intervened to disperse the gathering, it became a full-on riot with a number of casualties. Ironically, in commemoration of the rally, 1 May has come to be celebrated around the world as Labor Day—except as it turns out, in the United States, where Labor Day was pushed back to the first Monday in September and no law has ever been passed to limit the length of the workday.

While many of the movements that have challenged capitalism have emerged from, been based on, or allied with workers and labor unions, many others have not. Students may recognize the names of some of the early utopian socialists and utopian experiments (although you probably read about them in courses other than economics): Charles Fourier, Henri de Saint-Simon, Robert Owen, and Henry George. Beginning in the nineteenth century, in the United States and around the world, groups of individuals (often, but not always, influenced by various strands of socialist thinking) formed “intentional communities” and cooperative societies. The Shakers (in the United States) and Mondragón (in Spain) are perhaps the best known.

And the list of critics of capitalism—both individuals and movements—goes on. It includes, of course, a wide variety of left-wing populist, socialist, and communist political parties (some of which have come to power, either through democratic elections or revolutions). A fundamental questioning of the capitalist system has also emerged from and influenced many other individuals, groups, and traditions, from civil rights leaders (such as Martin Luther King, Jr., in the United States) and religious groups (for example, the liberation theologians in Latin America) to independence movements (Angola and Mozambique are cases in point) and transnational protests (like Occupy Wall Street).

What can we conclude from this brief survey? From the very beginning, both mainstream economic thought and capitalism have brought forth their critical others.

From the very beginning, the area of mainstream economics devoted to Third World development has been imbued with a utopian impulse. The basic idea has been that traditional societies need to be transformed in order to pass through the various stages of growth and, if successful, they will eventually climb the ladder of progress and achieve modern economic and social development.

Perhaps the most famous theory of the stages of growth was elaborated by Walt Whitman Rostow in 1960, as an answer to the following questions:

Under what impulses did traditional, agricultural societies begin the process of their modernization? When and how did regular growth become a built-in feature of each society? What forces drove the process of sustained growth along and determined its contours? What common social and political features of the growth process may be discerned at each stage? What forces have determined relations between the more developed and less developed areas?

Rostow’s model postulated that economic growth occurs in a linear path through five basic stages, of varying length—from traditional society through take-off and finally into a mature stage of high mass consumption.

While Rostow’s model and much of mainstream development theory can trace its origins back to Adam Smith—through the emphasis on increasing productivity, the expansion of markets, and the definition of development as the growth in national income—the development models that were prevalent in the immediate postwar period presumed that the pre-conditions growth were not automatic, but would have to be engineered through government intervention and foreign aid.

Mainstream modernization theory was created in the 1950s—and thus after the first Great Depression and World War II, when world trade had been severely disrupted, and in the midst of decolonization and the rise of the Cold War, when socialism and communism were attractive alternatives to many of the national liberation movements in the Global South. It was a determined effort, on the part of academics and policymakers in the United States and Western Europe, to showcase capitalist development and make the economic and social changes necessary in the West’s former colonies to initiate the transition to modern economic growth.*

The presumption was that government intervention was required to disrupt the economic and social institutions of so-called traditional society, in order to chart a path through the necessary steps to shift the balance from agriculture to industry, create national markets, build the appropriate physical and social infrastructure, generate a domestic entrepreneurial class, and eventually raise the level of investment and employ modern technologies to increase productivity in both rural and urban areas.

That was the time of the Big Push, Unbalanced Growth, and Import-Substitution Industrialization. Only later, during the 1980s, was development economics transformed by the successful pushback from the neoclassical wing of mainstream economics and free-market policymakers. The new orthodoxy, often referred to as the Washington Consensus, focused on privatizing public enterprises, eliminating government regulations, and the freeing-up of trade and capital flows.

Throughout the postwar period, mirroring the debates in mainstream microeconomic and macroeconomic theory, mainstream development theory has oscillated back and forth—within and across countries—between more public, government-oriented and more private, free-market forms of mainstream development theory and policy. And, of course, the ever-shifting middle ground. In fact, the latest fads within mainstream development theory combine an interest in government programs with micro-level decision-making. One of them focuses on local experiments—using either the randomized-control-trials approach elaborated by Abhijit Banerjee and Esther Duflo or the Millenium Villages Project pioneered by Jeffrey Sachs, which they use to test and implement strategies so that impoverished people in the Third World can find their own way out of poverty. The other is the discovery of the importance of “good” institutions—for example, by Daron Acemoglu—especially the delineation and defense of private-property rights, so that Rostow’s modern entrepreneurs can, with public guarantees but minimal interference otherwise, be allowed to keep and utilize the proceeds of their private investments.

The debates among and between the various views within mainstream development economics have, of course, been intense. But underlying their sharp theoretical and policy-related differences has been a shared utopianism based on the idea that modern economic development is equivalent to and can be achieved as a result of the expansion of markets, the creation of a well-defined system of private property rights, and the growth of national income. In the end, it is the same utopianism that is both the premise and promise of a long line of contributions, from Smith’s Wealth of Nations through Rostow’s stages of growth to the experiments and institutions of today’s mainstream development economists.

The alternatives to mainstream development also have a utopian horizon, which is grounded in a ruthless criticism of the theory and practice of the “development industry.”

One part of that critique, pioneered by among others Arturo Escobar (e.g., in his Encountering Development), has taken on the whole edifice of western ideas that supported development, which he and other post-development thinkers and practitioners regard as a contradiction in terms.** For them, development has amounted to little more than the West’s convenient “discovery” of poverty in the third world for the purposes of reasserting its moral and cultural superiority in supposedly post-colonial times. Their view is that development has been, unavoidably, both an ideological export (something Rostow would willingly have admitted) and a simultaneous act of economic and cultural imperialism (a claim Rostow rejected). With its highly technocratic language and forthright deployment of particular norms and value judgements, it has also been a form of cultural imperialism that poor countries have had little means of declining politely. That has been true even as the development industry claimed to be improving on past practice—as it has moved from anti-poverty and pro-growth to pro-poor and basic human needs approaches. It continued to fall into the serious trap of imposing a linear, western modernizing agenda on others. For post-development thinkers the alternative to mainstream development emerges from creating space for “local agency” to assert itself. In practice, this has meant encouraging local communities and traditions rooted in local identities to address their own problems and criticizing any existing distortions—both economic and political, national as well as international—that limit peoples’ ability to imagine and create diverse paths of development.

The second moment of that critique challenges the notion—held by mainstream economists and often shared by post-development thinkers—that capitalism is the centered and centering essence of Third World development. Moreover, such a “capitalocentric” vision of the economy has served to weaken or limit a radical rethinking of and beyond development.*** One way out of this dilemma is to recognize class diversity and the specificity of economic practices that coexist in the Third World and to show how modernization interventions have, themselves, created a variety of noncapitalist (as well as capitalist) class structures, thereby adding to the diversity of the economic landscape rather than reducing it to homogeneity. This is a discursive strategy aimed at rereading the economy outside the hold of capitalocentrism. The second strategy opens up the economy to new possibilities by theorizing a range of different and potential connections among and between diverse class processes. This forms part of a political project that can perhaps articulate with both old and new social movements in order to create new subjectivities and forge new economic and social futures in the Third World.

The combination of post-development and class-based anti-capitalocentric thinking refuses the utopianism of Third World development, as it constitutes a different utopian horizon—a critique of the naturalizing and normalizing strategies that are central to mainstream development theory and practice in the world today. It therefore leads in a radically different direction: to make noncapitalist class processes and projects more visible, less “unrealistic,” as one step toward dethroning the “development industry” and invigorating an economic politics beyond development.

*At the same time, the Western Powers attempted to reconstruct the global institutions of capitalism, through the triumvirate of the World Bank, the International Monetary Fund, and the General Agreement on Tariffs and Trade (predecessor to the World Trade Organization) that was initially hammered out in 1944 in the Bretton-Woods Agreement.

**A short reading list for the post-development critique of mainstream development includes the following: Wolfgang Sachs, ed., The Development Dictionary: A Guide to Knowledge As Power (Zed, 1992); Arturo Escobar, Encountering Development: The Making and Unmaking of the Third World (Princeton, 1995); Gustavo Esteva et al., The Future of Development: A Radical Manifesto (Policy, 2013); and the recent special issue of Third World Quarterly (2017), “The Development Dictionary @25: Post-Development and Its Consequences.”

***Building on a feminist definition of phallocentrism, I along with J.K. Gibson-Graham (in “‘After’ Development: Reimagining Economy and Class,” an essay published in my Development and Globalization: A Marxian Class Analysis) identify capitalocentrism whenever noncapitalism is reduced to and seen merely as the same as, the opposite of, the complement to, or located inside capitalism itself.

Mainstream economics lies in tatters. Certainly, the crash of 2007-08 and the Second Great Depression called into question mainstream macroeconomics, which has failed to provide a convincing explanation of either the causes or consequences of the most severe crisis of capitalism since the Great Depression of the 1930s.

But mainstream microeconomics, too, increasingly appears to be a fantasy—especially when it comes to issues of corporate power.

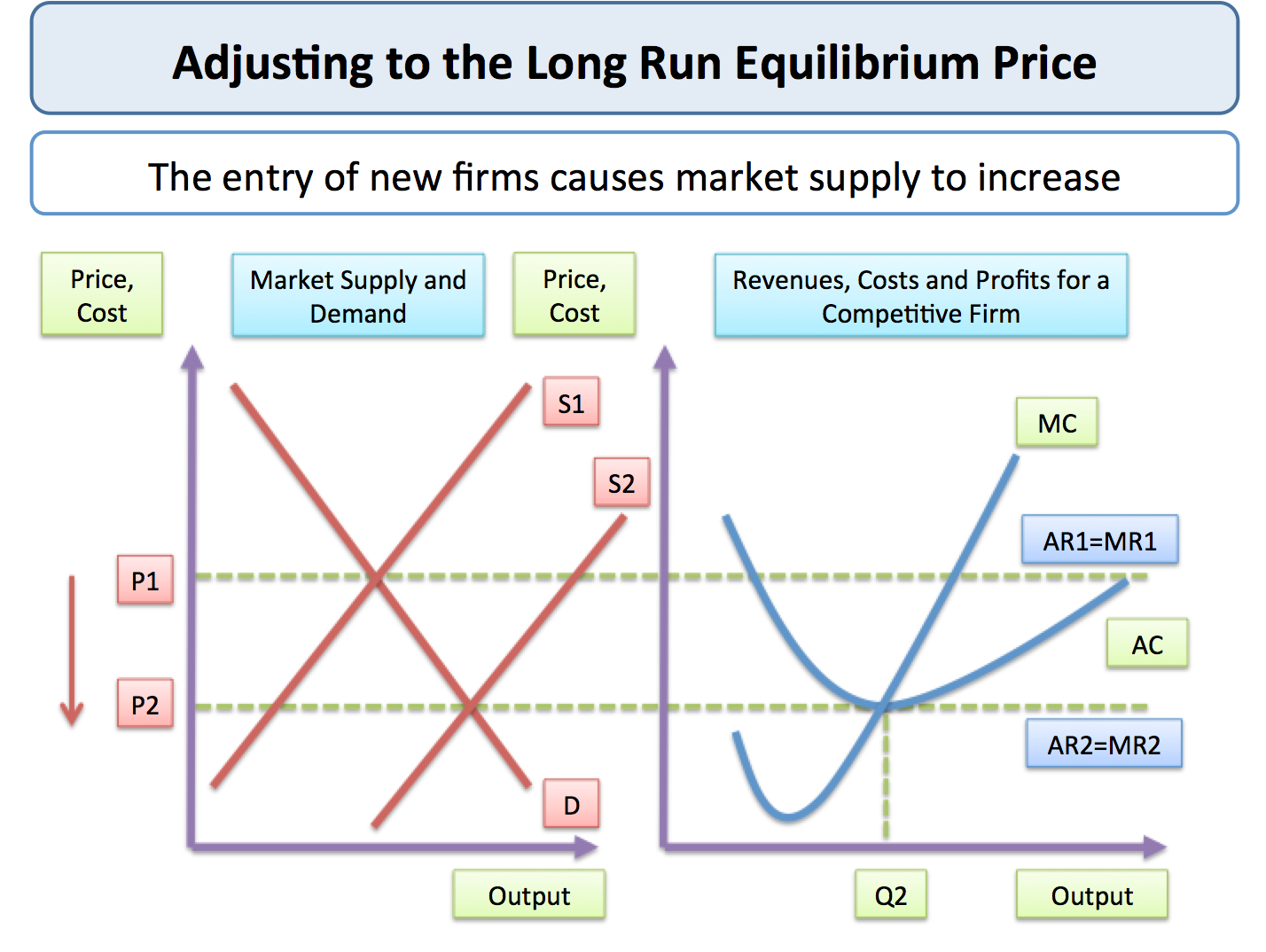

Neoclassical microeconomics is based on a set of models that assume perfect competition. What that means, as my students learned the other day, is that, while in the short run firms may capture super-profits (because price is greater than average total cost, at P1 in the chart above), in the “long run,” with free entry and exit, all those extra-normal profits are competed away (since price is driven down to P2, equal to minimum average total cost). That’s why the long run is such an important concept in neoclassical economic theory. The idea is that, starting with perfect competition, neoclassical economists always end up with. . .perfect competition.*

Except, of course, in the real world, where exactly the opposite has been occurring for the past few decades. Thus, as the authors of the new report from the United Nations Conference on Trade and Development have explained, there is a growing concern that

increasing market concentration in leading sectors of the global economy and the growing market and lobbying powers of dominant corporations are creating a new form of global rentier capitalism to the detriment of balanced and inclusive growth for the many.

And they’re not just talking about financial rentier incomes, which has been the focus of attention since the global meltdown provoked by Wall Street nine years ago. Their argument is that a defining feature of “hyperglobalization” is the proliferation of rent-seeking strategies, from technological innovations to mergers and acquisitions, within the non-financial corporate sector. The result is the growth of corporate rents or “surplus profits.”**

As Figure 6.1 shows, the share of surplus profits in total profits grew significantly for all firms both before and after the global financial crisis—from 4 percent during the 1995-2000 period to 19 percent in 2001-2008 and even higher, to 23 percent, in 2009-2015. The top 100 firms (ranked by market capitalization) also saw the growth of their surplus profits, from 16 percent to 30 percent and then, most recently, to 40 percent.***

The analysis suggests both that surplus profits for all firms have grown over time and that there is an ongoing process of bipolarization, with a growing gap between a few high-performing firms and a growing number of low-performing firms.

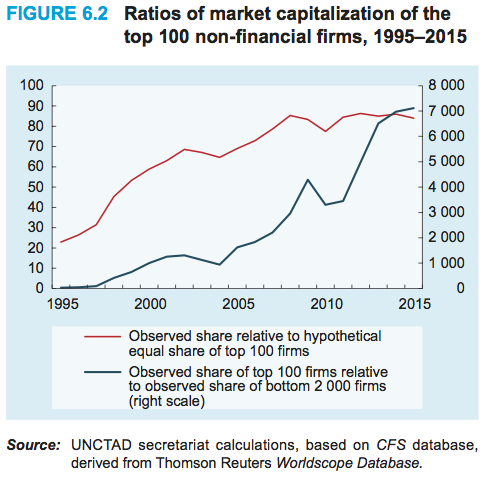

That conclusion is confirmed by their analysis of market concentration, which is presented in Figure 6.2 in terms of the market capitalization of the top 100 nonfinancial firms between 1995 and 2015. The red line shows the actual share of the top 100 firms relative to their hypothetical equal share, assuming that total market capitalization was distributed equally over all firms. The blue line shows the observed share of the top 100 firms relative to the observed share of the bottom 2,000 firms in the sample.

Both measures indicate that the market power of the top companies increased substantially over the 1995-2015 period. For example, the combined share of market capitalization of the top 100 firms was 23 times higher than the share these firms would have held had market capitalization been distributed equally across all firms. By 2015, this gap had increased nearly fourfold, to 84 times. This overall upward surge in concentration, measured by market capitalization since 1995, experienced brief interruptions in 2002−03 after the bursting of the dotcom bubble, and in 2009−2010 in the aftermath of the global financial crisis, and it stabilized at high levels thereafter.****

So, what is causing this growth in market concentration? One reason is because of the nature of the underlying technologies, which involve costs of production that do not rise proportionally to the quantities produced. Instead, after initial high sunk costs (e.g., in the form of expenditures on research and development), the variable costs of producing additional units of output are negligible.***** And then, of course, growing firms can use intellectual property rights and lobbying powers to protect themselves against actual or potential competitors.

Giant firms can also use their super-profits to merge with and to acquire other firms, a process that has accelerated because—as both a consequence and cause—of the weakening of antitrust legislation and enforcement.

What we’re seeing, then, is a “vicious cycle of underregulation and regulatory capture, on the one hand, and further rampant growth of corporate market power on the other.”

The models of mainstream economics turn out to be a shield, hiding and protecting this strengthening of corporate rule.

What the rest of us, including the folks at UNCTAD, have been witnessing in the real world is the emergence and consolidation of global rentier capitalism.

*There’s another reason why the long run is so important for neoclassical economists. All incomes are presumed to be returns to “factors of production” (e.g., land, labor, and capital), equal to their “marginal products.” But short-run super-profits are a theoretical embarrassment. They represent a return not to any factor of production but to something else: serendipity or Fortuna. Oops! That’s another reason it’s important, within a neoclassical world, for short-run super-profits to be competed away in the long run—to eliminate the existence of returns to the decidedly non-productive factor of luck.

**UNCTAD defines surplus profits as the difference between the estimate of total typical profits and the total of actually observed profits of all firms in the sample in that year. Thus, they end up with a lower estimate of surplus or super-profits than if they’d used a strictly neoclassical definition, which would compare actual profits to a zero-rent (or long-run equilibrium) benchmark.

***The authors note that

these results need to be interpreted with caution. More important than the absolute size of surplus profits for firms in the database in any given sub-period, is their increase over time, in particular the surplus profits of the top 100 firms.

****The authors of the study focus particular attention on the so-called high-tech sector, in which they show “a growing predominance of ‘winner takes most’ superstar firms.”

*****Thus, as Piero Sraffa argued long ago, the standard neoclassical model of perfect competition, with U-shaped marginal and average cost curves (i.e., “diminishing returns”), is called into question by increasing returns, with declining marginal and average cost curves.

I’m always pleased when Marx’s critique of political economy and the theory of value are topics of discussion, especially since students are rarely exposed to those ideas in their usual mainstream economics courses. Their professors generally don’t know about any theory of value other than the neoclassical economics they learned and preach—and, as a consequence, students aren’t taught that there is a fundamental critique of the neoclassical theory of value that stems from Marx’s work.

The result is, in fact, quite embarrassing. When I ask students to compare Marx’s theory of profits with the neoclassical theory of profits, they have no idea what I’m talking about. The way they learn economics from my neoclassical colleagues, profits are competed away. “So,” I ask them, “what you have is a theory of capitalism according to which there are no profits”? Then, of course, I have to start all over, teach them the neoclassical theory of profits (as the normal return to capital, rK, where r is the profit rate and K the amount of capital) and only then explain to them the Marxian critique of neoclassical profits (based on s, the amount of surplus-value that arises through exploitation). I am forced to make up for mainstream economists’ poor understanding and explanation of their own theory.

So, good, we now have a new discussion of Marx’s approach—first in the form of Branko Milanovic’s “primer” and then in Fred Moseley’s response to Milanovic. Both are well worth reading in their entirety—and I agree with many of the ideas they put forward.

But I do have a few major disagreements with their treatments. Milanovic, for example, insists that Marx develops his theory through three kinds of production: non-capitalism, “petty commodity production,” and capitalism. I read Marx differently. My view is that Marx starts with the commodity and then proceeds to develop, step by step (across volumes 1, 2, and 3 of Capital), the conditions of existence of capitalist commodity production, which is the goal of the analysis. These are not different historical stages or kinds of production but, rather, different levels of abstraction. So, conceptually, Marx starts from one proposition (that the value and exchange-value of commodities are equal to the amount of socially necessary abstract labor-time embodied in their production), then proceeds to another (where the value and exchange-value of commodities are equal to the value of capital, both variable and constant, and surplus-value embodied in the commodity during the course of production), and finally to a third level (where value and exchange-value can’t be equal, since the price of production, p, now includes an average rate of return on capital).

My other two concerns pertain to both authors. Milanovic and Moseley assert that Marx’s focus was mainly at the macro level, “the determination of the total profit (or surplus-value) produced in the capitalist economy as a whole.” I didn’t understand that idea back in 2013 and I remain unconvinced today. As I see it, Marx focused on both the micro and macro level and in fact worked to make his theory consistent at the two levels. Starting with the value of individual commodities (as I explained above), Marx concluded that, at the aggregate level, two identities needed to hold: the total value of commodities equaled the sum of their prices, and total surplus-value equalled total profits. That’s both a micro theory and a macro theory, a theory of value, price, and profit at both levels.*

The second, and perhaps most important, idea missing from Milanovic’s and Moseley’s interpretations of Marx’s approach is critique. Both authors proceed as if Marx developed his own theory of labor value, instead of seeing it as a critique of the classicals’ theory of value (which, we must remember, is the sub-title of Capital, “A Critique of Political Economy”). In my view, Marx begins where the classicals leave off (with an “immense accumulation of commodities,” Adam Smith’s wealth of nations) and then shows how the production of wealth in a capitalist society involves the performance, appropriation, and distribution of surplus labor.

That’s Marx’s class critique of political economy, which pertains as much to the mainstream economics of our time as to his.

*I don’t have the space here to explain how, for any individual commodity, the amount of value embodied during the course of its production won’t generally be equal to the amount of value for which the commodity exchanges. It is conceptually important that individual commodities have both numbers—value and exchange-value—attached to them, especially when they are not quantitatively equal at the micro level. It speaks to the fact that surplus-value is both appropriated (by capitalists from workers, through exploitation) and redistributed (among capitalists, within and across industries).

Plenty of illusions are being shattered these days, such as the idea that a successful recovery from the worst economic downturn since the Great Depression would keep the incumbents in power. A combination of lost jobs, stagnant wages, and soaring inequality put an end to that illusion. Much the same has happened to American Exceptionalism.

Noah Smith has just discovered another shattered illusion: the independence of supply and demand.

Mainstream economists generally think about the world in terms of supply and demand—at both the micro and macro levels: supply and demand in the market for oranges or labor (which determine the equilibrium price and quantity), as well as aggregate supply and demand for the economy as a whole (which determine the equilibrium level of prices and output). Perhaps even more important, they think about supply and demand as acting independently of one another: a shift in supply or demand in individual markets (which lead to changes in equilibrium prices and quantities) as well as “shocks” to aggregate supply or demand in macro models (which determine changes in the equilibrium level of prices and output). The presumption is that a shift in demand (at the level of individual markets or the economy as a whole) does not cause a shift in supply (at either level), or vice versa.*

As it turns out, the independence of supply and demand is just an illusion.

As I wrote back in 2009, it’s quite possible that at the micro level—for example, in the case of the labor market—both supply and demand are determined by something else, such as the accumulation of capital.

Thus. . .if the accumulation of capital leads to rightward shifts in both the demand for and supply of labor, wages may not increase (and quite possibly will decrease).

Therefore, supply and demand in individual markets aren’t necessarily independent.

And then, in 2013, I discussed the illusion of the independence of aggregate supply and demand.

In terms of the mainstream model, the collapse of aggregate demand leading to the crash of 2007-08 has also affected the aggregate supply of the economy—thereby shattering the illusion of the independence of the two sides of the macroeconomy. As the authors put it, “a significant portion of the recent damage to the supply side of the economy plausibly was endogenous to the weakness in aggregate demand—contrary to the conventional view that policymakers must simply accommodate themselves to aggregate supply conditions.”

Not only does the destruction of a significant portion of the future growth potential of the U.S. economy challenge the model mainstream economists use to analyze the macroeconomy and to formulate policy; it also forces us to question the rationality of a set of economic arrangements in which trillions of dollars of potential wealth (which might then be used to improve lives for the majority of the population) are sacrificed at the altar of keeping things pretty much as they are.

It represents the indictment both of an academic discipline and of economic system.

So, Smith is right: the shattering of the illusion of the independence of supply and demand means the way mainstream economists teach basic economics is fundamentally wrong.

What he forgets to mention, however, is that an economic system that is governed by supply and demand that are not independent of one another—and thus is subject to considerable instability on a regular basis, with the costs being shouldered by those who can least afford it—is also open to question.

Perhaps Tuesday’s results will serve notice that the time for challenging mainstream economics and the economic and social system celebrated by mainstream economists has finally arrived.

*There can, of course, be simultaneous shifts in supply and demand but the shifts themselves are considered independent of one another.

Yesterday, I explained that the 2016 Nobel Prize in Economics Bank of Sweden Prize in Economic Sciences in Memory of Alfred Nobel was awarded to Oliver Hart and Bengt Holmstrom because, through their neoclassical version of contract theory, they “proved” that capitalist firms—employers hiring labor to produce commodities in privately owned corporations—were the most natural, efficient way of organizing production.

It should come as no surprise, then, that mainstream economists—initially in tweets, then in full blog posts—have heaped praise on this year’s award.

Paul Krugman couldn’t believe Hart and Holmstrom hadn’t won the prize already, while Justin Wolfers considered them “an unarguably splendid pick.”

Tyler Cowen also expressed his conviction that the new Nobel laureates are “well-deserving economists at the top of the field.” (He then explains, in separate posts, the significance for neoclassical theory of Hart’s and Holmstrom’s research on the theory of the firm.) The other member of the Marginal Revolution team, Alex Tabarrock, follows up by criticizing the one instance in Hart’s work in which he actually criticizes private enterprise. Hart (in a piece with two other economists) argues one of the downsides of private prisons is that they sacrifice quality for cost—but, according to Tabarrock, “private prisons appear to be cheaper than public prisons but they are not significantly cheaper and the quality of private prisons is comparable to that of public prisons and maybe a little bit higher.”

And then there’s Noah Smith, who follows suit by praising “the new exciting tools that have been developed in the micro world,” including by the new Nobel laureates. He refers to that work in microeconomics as the “real engineering”—as against macroeconomics, “whose scientific value is still being debated.”

The fact is, the value of both areas of mainstream economics is still being debated, as it has been from the very beginning. There is nothing settled (except, perhaps, in the minds of mainstream economists) about either the theory of the firm or the causes of recessions and depressions, the determinants of a commodity’s value or the prospects for long-term capitalist growth, whether the labor market or the economy as a whole is in any kind of equilibrium.

Smith overlooks or ignores those debates, most of which occur between mainstream economists and other, nonmainstream heterodox economists. But then, in attempting to explain why this year’s prize went to microeconomists, Smith displays his real misunderstanding of the history of economics—arguing that “macro developed first.”

Economists saw big, important phenomena like growth, recessions and poverty happening around them, and they wrote down simple theories to explain what they saw. The theories started out literary, and became more mathematical and formal as time went on. But they had a few big things in common. They assumed the people and the companies in the economy were each very tiny and insignificant, like particles in a chemical solution. And they typically assumed that everyone follows very simple rules — companies maximize profits, consumers maximize the utility they get from consuming things. Pour all of these tiny simple companies and people into a test tube called “the market,” shake them up, and poof — an economy pops out.

Here’s the problem: macroeconomics didn’t develop first. Indeed, it wasn’t invented until the 1930s, when John Maynard Keynes published The General Theory of Employment, Interest, and Money. This should not be surprising, given the fact that the world was in the midst of the Great Depression, with at least 25 percent unemployment, after neoclassical microeconomists (following their classical predecessors, Adam Smith, David Ricardo, and Jean-Baptiste Say) had attempted to prove that markets would always be in equilibrium, which of course ruled out economic depressions and massive unemployment. Oops!

Since then, we’ve seen a mainstream tradition that combines (in different, shifting ways) neoclassical microeconomics and Keynesian macroeconomics—a tradition that failed miserably both in the lead-up to and following on the second Great Depression.

But no matter, at least from the perspective of mainstream economics, because its leading practitioners—sometimes from the macro side, this year from the micro side—continue, as if by contract, to be awarded Nobel prizes.

A constant refrain among mainstream economists and pundits since the crash of 2007-08 has been that, while the state of mainstream macroeconomics is poor, all is well within microeconomics.

The problems within macroeconomics are, of course, well known: Mainstream macroeconomists didn’t predict the crash. They didn’t even include the possibility of such a crash within their theory or models. And they certainly didn’t know what to do once the crash occurred.

What about microeconomics, the area of mainstream economics that was supposedly untouched by all the failures in the other half of the official discipline? Well, as it turns out, there are major problems there, too—especially given the obscene levels of inequality that both preceded and have resumed since the crash erupted, not to mention the slow economic growth that rising inequality was supposed to solve.

In particular, as I have written many times over the years, the idea that a rising tide lifts all boats—along with its theoretical justification, marginal productivity theory—needs to be questioned and ultimately abandoned.

But you don’t have to take my word for it. Just read the latest essay by Nobel Prize-winning economist Joseph Stiglitz.

Stiglitz first explains that neoclassical economists developed marginal productivity theory as a direct response to Marxist claims that the returns to capital are based on the exploitation of workers.

While exploitation suggests that those at the top get what they get by taking away from those at the bottom, marginal productivity theory suggests that those at the top only get what they add. The advocates of this view have gone further: they have suggested that in a competitive market, exploitation (e.g. as a result of monopoly power or discrimination) simply couldn’t persist, and that additions to capital would cause wages to increase, so workers would be better off thanks to the savings and innovation of those at the top.

More specifically, marginal productivity theory maintains that, due to competition, everyone participating in the production process earns remuneration equal to her or his marginal productivity. This theory associates higher incomes with a greater contribution to society. This can justify, for instance, preferential tax treatment for the rich: by taxing high incomes we would deprive them of the ‘just deserts’ for their contribution to society, and, even more importantly, we would discourage them from expressing their talent. Moreover, the more they contribute— the harder they work and the more they save— the better it is for workers, whose wages will rise as a result.

Then he argues that three striking aspects of the evolution of the United States and most other rich countries in the past thirty-five years—the increase in the wealth-to-income ratio, the stagnation of median wages, and the failure of the return to capital to decline—call into question the neoclassical story about the distribution of income.

Standard neoclassical theories, in which ‘wealth’ is equated with ‘capital’, would suggest that the increase in capital should be associated with a decline in the return to capital and an increase in wages. The failure of unskilled workers’ wages to increase has been attributed by some (especially in the 1990s) to skill-biased technological change, which increased the premium put by the market on skills. Hence, those with skills would see their wages rise, and those without skills would see them fall. But recent years have seen a decline in the wages paid even to skilled workers. Moreover, as my recent research shows, average wages should have increased, even if some wages fell. Something else must be going on.

As Stiglitz sees it, that “something else” is a combination of rent-seeking (especially land rents, intellectual property rents, and monopoly power) and increased exploitation (especially the weakening of workers’ bargaining power, based on weak unions and asymmetric globalization).*

The result is that the rising tide has only lifted a few boats at the top and left everyone else behind.

But Stiglitz is not done. He also explains that not only is growing inequality not necessary for growth; it actually has negative effects: it leads to weak aggregate demand (and, in an attempt to solve that problem, asset bubbles), less equality of opportunity (thus lowering growth in the future), and lower levels of public investment (since the rich believe they don’t need things like public transportation, infrastructure, technology, and education).

It should be noted that the existence of these adverse effects of inequality on growth is itself evidence against an explanation of today’s high level of inequality based on marginal productivity theory. For the basic premise of marginal productivity is that those at the top are simply receiving just deserts for their efforts, and that the rest of society benefits from their activities. If that were so, we should expect to see higher growth associated with higher incomes at the top. In fact, we see just the opposite.

Neoclassical marginal productivity theory was never a plausible explanation of the distribution of income in capitalist societies. And, as Stiglitz explains, it is even more questionable in light of the spectacular growth of inequality in recent decades.

The only conclusion is that we live in strange times—when the illusion of a rising tide that lifts all boats (and, with it, trickledown economics, “just deserts,” and the like) has been shattered, and yet mainstream economists continue to teach (and use as the basis of economic policy) its theoretical underpinnings, marginal productivity theory.

There’s nothing left but to declare that both mainstream macroeconomics and microeconomics—as basic theory and a guide for economic policy—have failed. There’s simply nothing there to be fixed. Both mainstream macroeconomics and microeconomics need to be set aside in favor of very different analyses and explanations of capitalist instability and inequality.

*Elsewhere (e.g., here, here, and here), I have raised questions about the rent-seeking argument and showed how it is different from the alternative, surplus-seeking explanation of inequality.

Today’s announcement that Angus Deaton was awarded the Nobel Prize in Economic Sciences was greeted in the usual fashion: plenty of versions of “a brilliant selection” (Tyler Cowen) and a few of the usual criticisms that economics is not really a science (Joris Luyendijk).

What I find interesting is that, like last year, the prize is given to a thoroughly mainstream economist—but Deaton’s work can be read as cutting against the grain of much of what has passed for mainstream economics over the years. Let me give a few examples:

First, Deaton spent a great deal of time trying to figure out how, at the microeconomic level, consumers distribute their spending among different goods. Basically, Deaton was telling his mainstream colleagues, “you just can’t assume demand curves are downward-sloping, for individuals and markets, and that actual consumer behavior is or is not consistent with the postulates of neoclassical utility-maximization, without actually measuring how consumers respond to changes in prices.”

Deaton’s work, at the macroeconomic level, was similar: he cast doubt on the existing mainstream theories concerning the relationship between consumption and income (based on representative-agent models) and suggested, once again, that it’s necessary to study how different consumers—some with falling incomes, others with rising incomes—actually respond to changes in incomes.

Third, Deaton used his work on demand and consumption to challenge facile models based on income per capita and exchange-rate-calculated comparisons of poverty across nations. He pioneered a consumption-based approach, based on cross-sectional surveys to determine actual consumption expenditures and levels of well-being, especially in Third World countries.

There’s no doubt that, in the end, Deaton’s work in challenging many of the existing theoretical and empirical models within mainstream economics—in the areas of microeconomics, macroeconomics, and development economics—were themselves firmly ensconced within and contributed to the further development of mainstream economics.

But the mainstream nature of that work has also permitted him to intervene in other debates, for example, concerning the effectivity of foreign aid (which, he argues, mostly helps keep nonpopular governments in power and does little to actually eliminate poverty), the role of poor health (which, as he sees it, is a result, not a cause, of poverty), and the current fascination with randomized trials (which fail to account for the causes of positive outcomes and, as a result, can’t be generalized to other problems and situations).

And, in the one previous mention of him on this blog, to sound a warning about growing inequality in the United States and other advanced countries:

The distribution of wealth is more unequal than the distribution of income, and very high incomes will eventually pupate into very large fortunes, ultimately leading to a hereditary dystopia of idle rich.