Posts Tagged ‘consumption’

Cartoons of the day

Posted: 9 September 2020 in UncategorizedTags: capitalism, cartoons, commodities, consumption, election, government, Trump, welfare

0

Billionaires—pandemic edition

Posted: 24 August 2020 in UncategorizedTags: Amazon, Apple, billionaires, China, conspicuous consumption, consumption, coronavirus, Facebook, fascism, Google, Microsoft, pandemic, robber barons, safety, unemployment, United, wealth, world

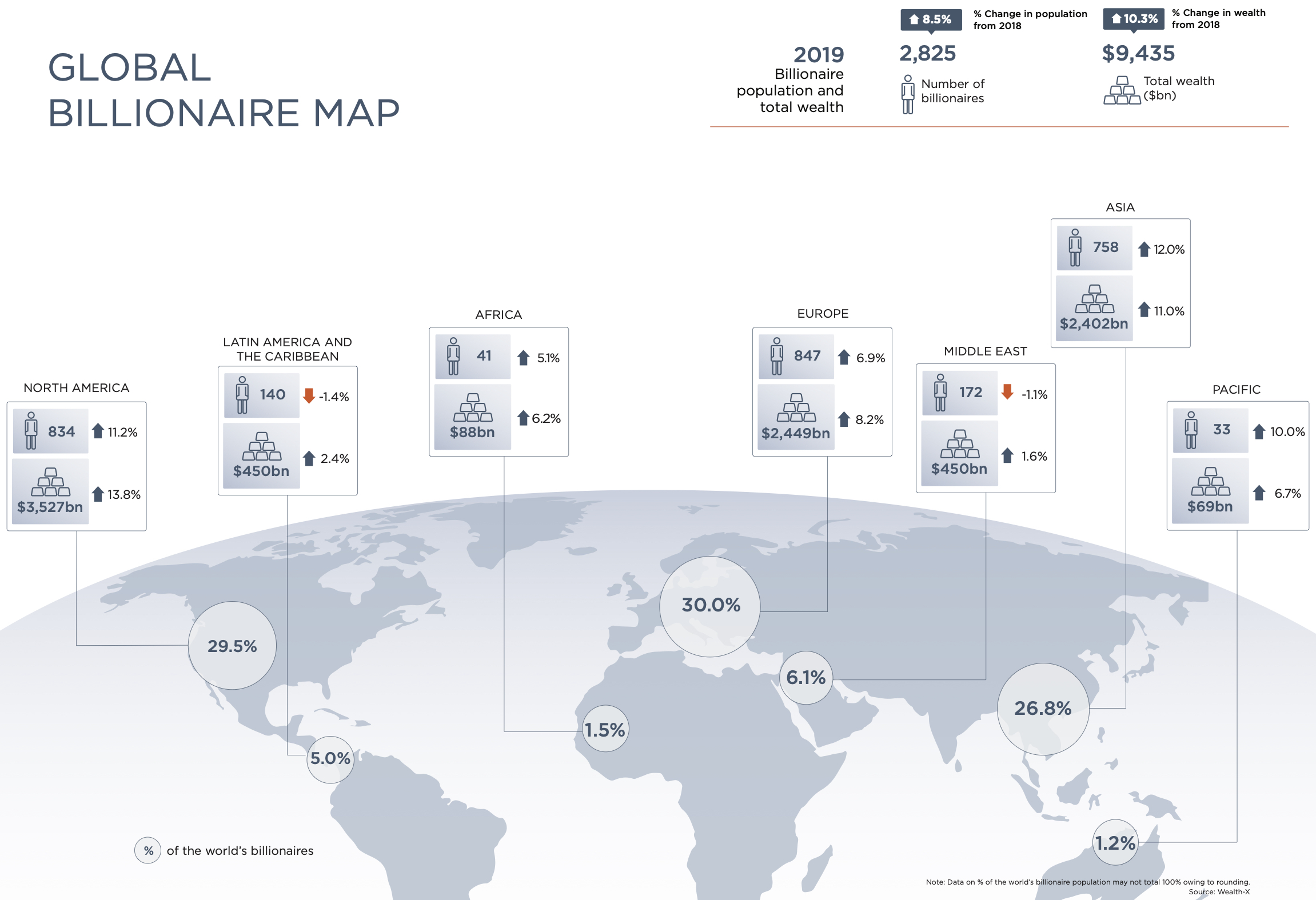

2019 was a very good year for the world’s wealthiest individuals. The normal workings of global capitalism created both more billionaires and more combined wealth owned by those billionaires.

According to Wealth-X, which claims to “have developed the world’s most extensive collection of records on wealthy individuals and produce unparalleled data analysis to help our clients uncover, understand, and engage their target audience, as well as mitigate risk,” the size of the global billionaire population increased strongly in 2019, rising by 8.5 percent

to 2,825 individuals, while their combined wealth increased by 10.3 percent to $9.4 trillion.

To put that into perspective, the world’s real Gross Domestic Product grew by only 2.9 percent (International Monetary Fund) in 2019—while the value of global equities, which is key to billionaires’ wealth, soared by more than 25 percent (MSCI World Index).

The United States still leads the list of the world’s billionaire population and their wealth. In 2019, the number of American billionaires rose by almost 12 percent to 788 individuals, accounting for 28 percent of the global billionaire population (China has the next highest share at 12 percent). Cumulative billionaire wealth in the United States increased by 14 percent to $3.4 trillion, more than the combined net worth of the next eight highest-ranked countries and equivalent to a 36 percent share of global billionaire wealth.*

What about the novel coronavirus pandemic?

According to Bloomberg, only two of the world’s 10 richest people have seen their wealth decline in 2020: luxury mogul Bernard Arnault and Berkshire Hathaway Inc.’s Warren Buffett. Everyone else, whose wealth is tied to technology holdings (except for Mukesh Ambani, the Indian billionaire who chairs and runs oil and gas giant Reliance Industries), has seen their individual and collective wealth increase—none more so than Jeff Bezos (the Amazon.com Inc. founder who has seen his net worth soar by $63.6 billion this year) and Elon Musk (whose net worth has more than doubled to $69.7 billion on the back of surging Tesla Inc shares).**

On a global level, billionaires tied to technology businesses have outperformed all others, especially those whose wealth is tied to the automotive, shipping, media, textiles and apparel, and aerospace (less so defense) industries. They, of course, are the ones who most want to see a quick solution to the pandemic and a reopening of economic activity around the world.

In general terms, wealthier billionaires are more exposed to the ebbs and flows of the stock market, while those at lower tiers tend to have more of their wealth in private holdings, likely to be their primary business. For example, those in the two highest billionaire wealth tiers—above $10 billion— hold between almost half and more than three-quarters of their assets in public holdings. These individuals have withstood significant volatility in their wealth as stock markets first fell considerably and then rebounded equally dramatically—this past Friday, to a new record high in the United States—since the beginning of the pandemic.

So, what are the world’s billionaires, in the United States and around the globe, doing with their wealth in the midst of the pandemic? We know they’re not particularly worried with the same problems as their predecessors, the Robber Barons, whose enormous economic power in the United States created a fierce counter-reaction, in militant labor unrest and the adoption of reforms that once seemed radical, like the Sherman Antitrust Act and a federal income tax.

At least so far. . .

Instead, according to Wealth-X, they are

working with their wealth advisors and planners to ensure their financial holdings and wealth plans (whether concerned with investment diversification, wealth transfer or philanthropic aims) remain up to date and in the best possible state given the evolving global situation.

They’re also concerned about their own safety and new forms of luxury consumption. According to the Wealth-X Global Luxury Outlook 2020. “The wealthy’s mindset around what luxury is has changed—their priorities have shifted towards their families,” Jaclyn Sienna India, CEO of luxury travel company Sienna Charles, said in the report. “Luxury now includes a second passport, access to healthcare and the freedom to go when and where they feel safe and secure.”

“Quite a few wealthy people are looking for exclusive safe havens in the form of second homes—safety has become a priority for them,” Alistair Brown, CEO of Alistair Brown International Real Estate. “But with this purchase, they expect access to established locations often via residency and additional passports as well as access to medical help.”

Additionally, the wealthy have become increasingly accustomed to purchasing luxury goods online since the pandemic, as high-end brands expand their digital offerings, the report said.

“The wealthy continue to value luxury as they did prior to Covid-19. However, the way they buy luxury has changed, with more having moved to making their purchases online,” Winston Chesterfield, principal of luxury watch company Barton.

Meanwhile, what is everyone else supposed to do? Well, they have to stay as safe as they can at home and on the job—as they are subjected to the second or third wave of the pandemic—and try to obtain sufficient food, remain in their shelter while not being able to keep up with their rents and mortgages, and pay for their healthcare—in the midst of widespread pay cuts and soaring unemployment.

And, perhaps, begin to sharpen the twenty-first century equivalent of pitchforks. . .

———

*That’s my quick (and, I understand, overly simplistic) argument against the rise of fascism in the United States: billionaires and the other members of the group of ultra-wealthy individuals don’t need it, since they’re doing quite well the way things are.

**Currently, five of the largest American tech companies—Apple, Amazon, Alphabet, Facebook, and Microsoft—have market valuations equivalent to about 30 percent of U.S. gross domestic product. That’s almost double what they were at the end of 2018.

Cartoon of the day

Posted: 25 November 2019 in UncategorizedTags: capitalism, cartoon, colonialism, consumption, globalization, impeachment, Trump

Special mention

Cartoon of the day

Posted: 12 September 2019 in UncategorizedTags: cartoon, consumption, debt, guns, inequality, John Bolton, student debt, trade, Trump, United States, violence, wages, wealth

Special mention

Cartoon of the day

Posted: 12 June 2019 in UncategorizedTags: cartoon, consumption, equality, fascism, football, Italy, soccer, student debt, students, United States, women

Special mention

Cartoon of the day

Posted: 24 October 2018 in UncategorizedTags: capitalism, cartoon, consumption, GOP, Republicans, Saudi Arabia, tax cuts, Trump

Special mention

Cartoon of the day

Posted: 25 January 2018 in UncategorizedTags: cartoon, commodities, consumption, corporations, exploitation, ICE, immigrants, immigration, prisons, racism, United States

Special mention

Trumponomist

Posted: 6 March 2017 in UncategorizedTags: 1 percent, consumption, corporations, DJIA, economists, Greg Mankiw, income, inequality, Kevin Hassett, mainstream, taxes, Trump, wealth, workers

According to recent news reports, Kevin Hassett, the State Farm James Q. Wilson Chair in American Politics and Culture at the American Enterprise Institute (no, I didn’t make that up), will soon be named the head of Donald Trump’s Council of Economic Advisers.

Yes, that Kevin Hassett, the one who in 1999 predicted the Down Jones Industrial Average would rise to 36,000 within a few years.

Except, of course, it didn’t. Not by a long shot. The average did reach a record high of 11,750.28 in January 2000, but after the bursting of the dot-com bubble, it steadily fell, reaching a low of 7,286 in October 2002. Although it recovered to a new record high of 14,164 in October 2007, it crashed back to the vicinity of 6,500 by the early months of 2009. And, even today, almost two decades later, it’s only just cracked the 20,000 barrier.

But, no matter, mainstream economists and pundits—like Greg Mankiw, Noah Smith, and Tim Worstall—think Hassett is a great choice.

Perhaps, in addition to his Dow book, they want to place the rest of Hassett’s writings on an altar.

Like Hassett’s claim (which I discuss here) that “lowering corporate taxes is the only real cure for wage stagnation among American workers.”

Or his other major claim (which I discuss here), that poverty and inequality in the United States are merely figments of our imagination.

Let’s focus on that last claim. As regular readers of this blog know, income inequality—whether measured in terms of fractiles (e.g., the 1 percent versus everyone else) or classes (e.g., profits and wages)—has been increasing for decades now. But for conservative economists like Hassett (who was an economic adviser to Mitt Romney before being a candidate to join the Trump team), inequality has not been growing and poor people are actually much better off than they and the rest of us normally think. What they do then is substitute consumption for income and argue that consumption inequality has actually not been growing.

So, what’s the big problem?

But even in terms of consumption they’re wrong. As Orazio Attanasio, Erik Hurst, Luigi Pistaferri have shown, once you correct for the measurement errors in the Consumer Expenditure Survey (which Hassett and his coauthor, Aparna Mathur, don’t do), and bring in other sources of consumption information (including the well-regarded Panel Study of Income Dynamics), consumption inequality has increased substantially in recent decades—more or less at the same rate as inequality in the distribution of income.

Overall, our results suggest that there has been a substantial rise in consumption and leisure inequality within the U.S. during the last 30 years. The rise in income inequality translated to an increase in actual well-being inequality during this time period because consumption inequality also increased.

And, remember, that doesn’t take into account other forms of inequality, such as the increase in the unequal distribution of wealth, which has exploded in recent decades. The poor and pretty much everyone else—the 90 percent—are being left behind.

It’s the spectacular grab for income, consumption, and wealth by the small group at the top that Hassett and the new administration will be trying to protect.

Blame globalization?

Posted: 15 November 2016 in UncategorizedTags: automation, consumption, election, imports, jobs, minimum wage, outsourcing, technology, Trump, unions, United States, wages, workers, working-class

Chris Dillow is right about one thing: citing globalization as the reason for the success of Donald Trump’s campaign, especially among working-class voters, “suits some people very well for foreigners to get the blame rather than for inequality and the health of capitalism to come under scrutiny.”

But that doesn’t mean that, alongside many other factors (from the decline in labor unions to increasing automation), globalization—to be precise, capitalist globalization—doesn’t deserve some good share of the blame.

There are two main ways the U.S. working-class is affected by globalization: in terms of jobs and in terms of consumption.

As far as jobs are concerned, the combination of cheap imports (e.g., toys and garments) and outsourcing (e.g., to produce motor vehicles and electronics) has led to the reallocation of workers away from high-wage manufacturing jobs into other sectors and occupations, with large declines in wages among workers who have been forced to have the freedom to switch. Those effects are pretty straightforward, at least in terms of the research of Avraham Ebenstein, Ann Harrison, and Margaret McMillan.*

What about the cheaper goods workers can buy? The argument that is usually invoked to counter the negative effects on jobs and wages is that workers can now purchase less expensive goods (e.g., at big-box and dollar stores), thereby increasing their consumption.

Here’s Dillow:

For one thing, cheap imports should help workers. If you’re spending $5 on a Chinese T-shirt rather than $10 on a US-made one, you’ve got $5 more to spend on other things. That should increase demand and jobs.

That may be true in the short run, since with the same nominal incomes workers can add other items to their consumption bundle.

But what Dillow and others miss is the fact that, as the prices of items in the wage bundle decline (and without an ability to defend the value of their customary standard of living), the value of workers’ labor power also has a tendency to decline. As a result, employers have to pay less to get access to laborers’ ability to work—and their profits rise.

Considering both jobs and consumption, members of the U.S. working-class—many of them voters in Pennsylvania, Ohio, Michigan, and Wisconsin—correctly understood they were under assault by the forces of globalization.

The fact that U.S. workers have, in recent decades, been negatively affected by globalization doesn’t mean either adopting a nationalist stance or ignoring all the other factors. Nationalism (e.g., in terms of erecting protectionist barriers to trade) just pits workers in one country against those in other countries and doesn’t, within any country including the United States, solve the problem of workers getting the short end of the economic stick. And, certainly, we need to look at all the causes of workers’ current plight, from deteriorating real minimum wages to skill- and power-biased technological change.

However, globalization as it is currently configured has been one of the strategies employers have been able to use to discipline and punish workers, increasing both inequality and insecurity.

Globalization is therefore at least in part to blame for Trump’s victory.

*Even those who, like Gary Clyde Hufbauer and Tyler Moran, want to argue that, through the “prosperity effect,” globalization has made a positive contribution to average wages, are forced to admit that “Richer households did enjoy a disproportionate share of benefits from globalization, because of their dominant claim on corporate profits and proprietors’ incomes and the very small impact of foreign competition on the wages of highly skilled workers.”

Interpret this!

Posted: 12 August 2016 in UncategorizedTags: capitalism, consumption, economics, heterodox, Hyman Minsky, investment, macroeconomics, mainstream, Marx, mathematics, models, profits

I know I shouldn’t. But there are so many wrong-headed assertions in the latest Bloomberg column by Noah Smith, “Economics Without Math Is Trendy, But It Doesn’t Add Up,” that I can’t let it pass.

But first let me give him credit for his opening observation, one I myself have made plenty of times on this blog and elsewhere:

There’s no question that mainstream academic macroeconomics failed pretty spectacularly in 2008. It didn’t just fail to predict the crisis — most models, including Nobel Prize-winning ones, didn’t even admit the possibility of a crisis. The vast majority of theories didn’t even include a financial sector.

And in the deep, long recession that followed, mainstream macro theory failed to give policymakers any consistent guidance as to how to respond. Some models recommended fiscal stimulus, some favored forward guidance by the central bank, and others said there was simply nothing at all to be done.

It is, in fact, as Smith himself claims, a “dismal record.”

But then Smith goes off the tracks, with a long series of misleading and mistaken assertions about economics, especially heterodox economics. Let me list some of them:

- citing a mainstream economist’s characterization of heterodox economics (when he could have, just as easily, sent readers to the Heterodox Economics Directory—or, for that matter, my own blog posts on heterodox economics)

- presuming that heterodox economics is mostly non-quantitative (although he might have consulted any number of books by economists from various heterodox traditions or journals in which heterodox economists publish articles, many of which contain quantitative—theoretical and empirical—work)

- equating formal, mathematical, and quantitative (when, in fact, one can find formal models that are neither mathematical nor quantitative)

- also equating nonquantitative, broad, and vague (when, in fact, there is plenty of nonquantitative work in economics that is quite specific and unambiguous)

- arguing that nonquantitative economics is uniquely subject to interpretation and reinterpretation (as against, what, the singular meaning of the Arrow-Debreu general equilibrium system or the utility-maximization that serves as the microfoundations of mainstream macroeconomics?)

- concluding that “heterodox economics hasn’t really produced a replacement for mainstream macro”

Actually, this is the kind of quick and easy dismissal of whole traditions—from Karl Marx to Hyman Minsky—most heterodox economists are quite familiar with.

My own view, for what it’s worth, is that there’s no need for work in economics to be formal, quantitative, or mathematical (however those terms are defined) in order for it be useful, valuable, or insightful (again, however defined)—including, of course, work in traditions that run from Marx to Minsky, that focused on the possibility of a crisis, warned of an impending crisis, and offered specific guidances of what to do once the crisis broke out.

But if Smith wants some heterodox macroeconomics that uses some combination of formal, mathematical, and quantitative techniques he need look no further than a volume of essays that happens to have been published in 2009 (and therefore written earlier), just as the crisis was spreading across the United States and the world economy. I’m referring to Heterodox Macroeconomics: Keynes, Marx and Globalization, edited by Jonathan P. Goldstein and Michael G. Hillard.

There, Smith will find the equation at the top of the post, which is very simple but contains an idea that one will simply not find in mainstream macroeconomics. It’s merely an income share-weighted version of a Keynesian consumption function (for a two-class world), which has the virtue of placing the distribution of income at the center of the macroeconomic story.* Add to that an investment function, which depends on the profit rate (which in turn depends on the profit share of income and capacity utilization) and you’ve got a system in which “alterations in the distribution of income can have important and potentially offsetting impacts on the level of effective demand.”

And heterodox traditions within macroeconomics have built on these relatively simply ideas, including

a microfounded Keynes–Marx theory of investment that further incorporates the external financing of investment based upon uncertain future profits, the irreversibility of investment and the coercive role of competition on investment. In this approach, the investment function is extended to depend on the profit rate, long-term and short-term heuristics for the firm’s financial robustness and the intensity of competition. It is the interaction of these factors that fundamentally alters the nature of the investment function, particularly the typical role assigned to capacity utilization. The main dynamic of the model is an investment-induced growth-financial safety tradeoff facing the firm. Using this approach, a ceteris paribus increase in the financial fragility of the firm reduces investment and can be used to explain autonomous financial crises. In addition, the typical behavior of the profit rate, particularly changes in income shares, is preserved in this theory. Along these lines, the interaction of the profit rate and financial determinants allows for real sector sources of financial fragility to be incorporated into a macro model. Here, a profit squeeze that shifts expectations of future profits forces firms and lenders to alter their perceptions on short-term and long-term levels of acceptable debt. The responses of these agents can produce a cycle based on increases in financial fragility.

It’s true: such a model does not lead to a specific forecast or prediction. (In fact, it’s more a long-term model than an explanation of short-run instabilities.) But it does provide an understanding of the movements of consumption and investment that help to explain how and why a crisis of capitalism might occur. Therefore, it represents a replacement for the mainstream macroeconomics that exhibited a dismal record with respect to the crash of 2007-08.

But maybe it’s not the lack of quantitative analysis in heterodox macroeconomics that troubles Smith so much. Perhaps it’s really the conclusion—the fact that

The current crisis combines the development of under-consumption, over-investment and financial fragility tendencies built up over the last 25 years and associated with a finance-led accumulation regime.

And, for that constellation of problems, there’s no particular advice or quick fix for Smith’s “policymakers and investors”—except, of course, to get rid of capitalism.

*Technically, consumption (C) is a function of the marginal propensity to consume of labor, labor’s share of income, the marginal propensity to consume of capital, and the profit share of income.