Special mention

Special mention

Special mention

Special mention

Mark Tansey, “Garden” (2006)

Modern Monetary Theorists are having a moment, as governments (many of them run by conservative regimes, such as Donald Trump and the Republicans in the United States) are running gigantic fiscal deficits in order to combat the economic crisis occasioned by the coronavirus pandemic.*

This time, with the $2 trillion CARES Act, the U.S. federal government has taken an additional step down the road of Modern Monetary Theory, by having the Federal Reserve buy an unlimited amount of Treasury bonds and government-backed mortgage bonds — whatever was necessary “to support smooth market functioning”—in other words, by simply creating the necessary money.

But, as Michael Hudson et al. explain, the idea that is being celebrated right now—that running government budget deficits is stabilizing instead of destabilizing—”is in many ways something quite different than the leading MMT advocates have long supported.”

Modern Monetary Theory (MMT) was developed to explain the logic of running government budget deficits to increase demand in the economy’s consumption and capital investment sectors so as to maintain full employment. But the enormous U.S. federal budget deficits from the Obama bank bailout after the 2008 crash through the Trump tax cuts and Coronavirus financial bailout have not pumped money into the economy to finance new direct investment, employment, rising wages and living standards. Instead, government money creation and Quantitative Easing have been directed to the finance, insurance and real estate (FIRE) sectors. The result is a travesty of MMT, not its original aim.

By subsidizing the financial sector and its debt overhead, this policy is deflationary instead of supporting the “real” economy. The effect has been to empower the banking sector, whose product is credit and debt creation that has taken an unproductive and indeed extractive form.

Let me back up for a moment. I’ve been an advocate of Modern Monetary Theory ever since I began to study it (at the prodding of friends [ht: br]), as can be seen in various of my blog posts. In particular, from the perspective of the Marxian critique of political economy, two formulations that represent both critiques of and alternatives to those of mainstream economics are particularly useful: government deficits and bank money.

Perhaps the best known (and, in many ways, most controversial) aspect of Modern Monetary Theory is the logic of running budget deficits. The mainstream view is that the government imposes taxes and then uses the revenues to pay for some portion of government programs. To pay for the rest of its expenditures, the state then borrows money by issuing bonds that investors can purchase (and for which they receive interest payments).** But, neoclassical economists complain, such borrowing has a big downside: budget deficits increase the demand for loans, because the government competes with all the loans that private individuals and businesses want to take on—thus leading, in the short run, to the so-called crowding-out effect and, in the long run, an increase in government debt and the potential for a government default.

Advocates of Modern Monetary Theory dispute both of these conclusions: First, they argue that governments should never have to default so long as the country has a sovereign currency, that is, so long as they issue and control the kind of money they tax and spend (so, e.g., the United States but not Greece). Second, taxes and bonds do not and indeed cannot directly pay for spending. Instead, the government creates money whenever it spends.*** Clearly, this is useful from a left-wing perspective, because it creates room for government spending on programs that benefit the working-class—including, but certainly not limited to, the much-vaunted jobs guarantee.****

The second major contention between mainstream economics and Modern Monetary Theory concerns the role of banks—in particular, the relationship between bank lending and money. As Bill Mitchell explains,

Mainstream economic theory considers banks to be institutions that take in deposits which then provides them with the funds to on-lend at a profit. Accordingly, the ability of private banks to lend is considered to be constrained by the reserves they hold.

In other words, banks are seen as financial intermediaries, funneling deposits and then (backed by reserves) allocating a multiple of such deposits to the best possible, most efficient uses.

From the perspective of Modern Monetary Theory, private banks don’t operate in this way. Instead, they create money, by making loans—and reserve balances play little if any role.

A bank’s ability to expand its balance sheet is not constrained by the quantity of reserves it holds or any fractional reserve requirements. The bank expands its balance sheet by lending. Loans create deposits which are then backed by reserves after the fact. The process of extending loans (credit) which creates new bank liabilities is unrelated to the reserve position of the bank.

This is exactly the opposite of the mainstream story, with the implication that banks create loans (and therefore money) based on the profitability of making such loans, an activity that has nothing to do with the central bank’s adding more reserves to the system.

Both points—concerning the financing of government spending and endogenous bank money—are well known to anyone who has been exposed (either sympathetically or critically) to Modern Monetary Theory. In my view, they fit usefully and relatively easily into modern Marxian economics, especially in terms of both the theory of the state (e.g., government finances) and the theory of (fiat) money.

The problem, it seems to me, arises in the terms of the major complaint registered by Hudson et al.—namely, that government stimulus plans have mostly been directed to the finance, insurance and real estate (FIRE) sectors, which are considered unproductive and extractive, and not to the “real” economy, which is not.

Readers who know something about the history of economic thought will recognize that these productive/unproductive and extractive/non-extractive distinctions have a long lineage and can be traced back, first, to the French Physiocrats and, later, to Adam Smith—in other words, to the beginnings of modern mainstream economics.

Using his Tableau Économique, François Quesnay attempted to show that the proprietors and cultivators of land were the only productive members of the economy and society, as against the unproductive class composed of manufacturers and merchants. It follows that the government should promote the interests of the landowners, and not those of the other classes, which were merely parasitic. Smith took up this distinction but then redeployed it, to argue that any labor involved in the production of commodities (whether agricultural or manufacturing) was productive, and the problem was with revenues spent on unproductive labor (such as household servants and landlords). The former led to the accumulation of capital, which increased the wealth of nations, while the latter represented conspicuous consumption, which did not.

Marx criticized both formulations, arguing that the productive/unproductive distinction had to do not with what workers produced, but rather with how they produced. Within capitalism, labor was productive if it resulted in the creation of surplus-value; and, if it didn’t (such as is the case with managers and CEOs who supervise the production of goods and services, as well as all those involved in finance, insurance, and real estate), it was not. So, the Marxian distinction is focused on surplus-value and thus exploitation.

And that, it seems to me, is the major point overlooked in much of Modern Monetary Theory. FIRE is extractive in the sense that it receives a cut of the surplus created elsewhere in the economy. But so are industries outside of finance, insurance, and real estate, since the boards of directors of enterprises in those sectors extract surplus from their own workers. And those different modes of extraction occur whether or not there’s a jobs guarantee provided by the creation of money by governments or banks.

From a Marxian perspective, then, the crucial distinction—both theoretically and for public policy—is not that between FIRE and the so-called real economy, but between classes that appropriate the surplus and otherwise “share in the booty” and the class that actually produces the surplus.

Right now, in the midst of the coronavirus pandemic, the class that is working to produce the surplus and provide the commodities we need is the one that is carrying the burden—either because they have been laid off and mostly left to their own devices, without paychecks and healthcare benefits, or been forced to continue to labor under precarious and unsafe conditions.

It’s that class, the American working-class, that is suffering from the ravages of the current economic crisis precipitated by the pandemic. They’re the ones, not their employers (whether in FIRE or the “real” economy), who deserve to be bailed out.

*Although this is certainly not the first time Republican administrations have run fiscal deficits, and allowed the public debt to soar—as long as they’re in power. They did it under Ronald Reagan, both Bushes, and long before the pandemic with Trump’s tax cuts. The only time American conservatives seem to worry about deficits and debt is when Democrats hold the reins.

**Wealthy individuals and large corporations long ago determined they prefer to be paid to purchase government debt instead of being taxed.

***So why, then, does the government need to tax at all in Modern Monetary Theory? Best I can figure, there are two major reasons: First, taxation makes sure people in the country use the government-issued currency, because they have to pay taxes in that currency (and not, e.g., in some kind of local or digital currency). Second, taxes are one tool governments can use to control inflation. They can take an amount of money out of the economy, which keeps consumers and corporations from bidding up prices.

****But that’s clearly not a new idea. Back in 1943, Michel Kalecki argued that governments had the ability to use a spending program (e.g., through public investment or subsidizing mass consumption) to achieve full employment. But it would likely be opposed by an alliance of big business and rentier interests based on three reasons:

(i) dislike of government interference in the problem of employment as such; (ii) dislike of the direction of government spending (public investment and subsidizing consumption); (iii) dislike of the social and political changes resulting from the maintenance of full employment.

In other words, capitalists are against both the government’s usurping of their private role as masters of the economy and society and the strengthening of the working-class, for whom “the ‘sack’ would cease to play its role as a disciplinary measure.”

Special mention

Special mention

Special mention

Special mention

Special mention

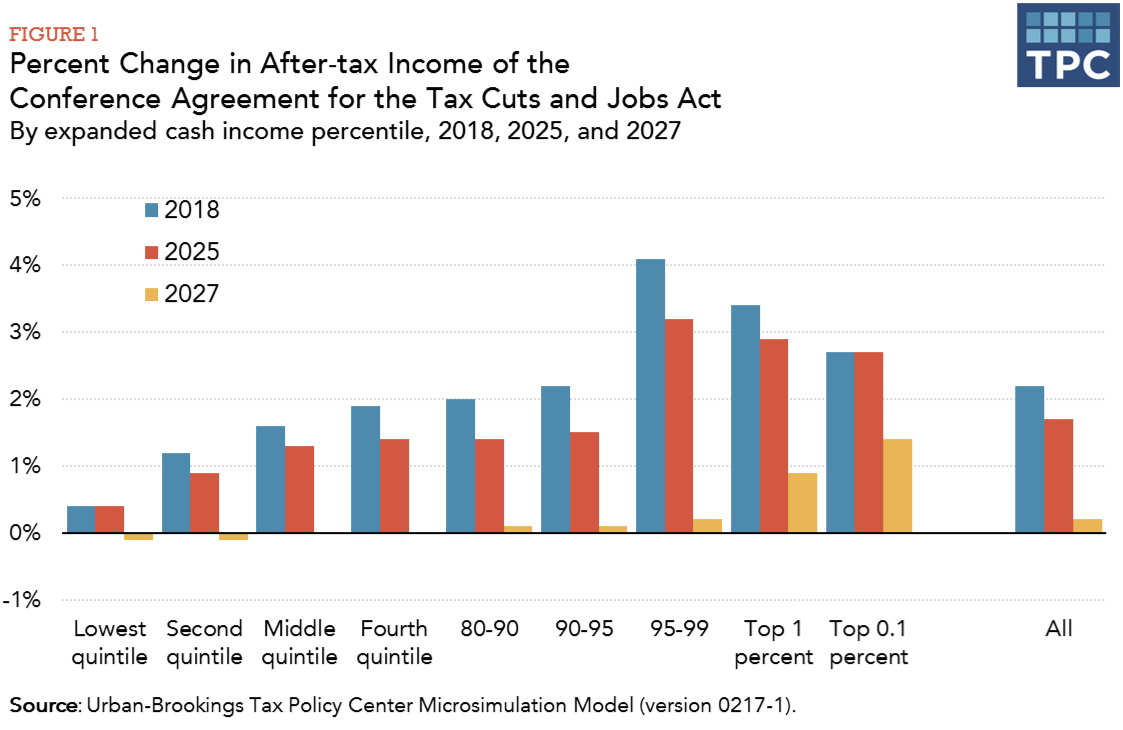

Tax cuts and spending increases enacted by Republicans over the past four months will lead to wider than previously expected budget deficits, according to the Congressional Budget Office. The federal budget deficit would total $804 billion this year, 43 percent higher than it had projected last summer, and exceed $1 trillion a year starting in 2020.

Larger deficits will, of course, add to the national debt: debt held by the public will hit $28.7 trillion at the end of fiscal 2028, or 96.2 percent of gross domestic product, up from 78 percent of GDP in 2018.

Those estimates assume current law will remain in effect, meaning Congress would allow some tax cuts to expire and spending caps to take effect again in the coming years. If Congress extends the tax cuts, as many Republicans want to do, the CBO predicted higher deficits and publicly held debt of about 105 percent of GDP by the end of 2028—a level exceeded only once in U.S. history, in the immediate aftermath of World War II.

So, what do these escalating deficit and debt numbers mean?

Clearly, in the first instance, the Republican deficit hawks have gone the way of moderate Republicans and all other extinct species of politicians and other mammals. They existed for decades, always in an attempt to cut entitlement programs and other public expenditures for poor and working-class Americans. But once it was possible to pass massive tax cuts for corporations and wealthy individuals and boost military spending, the deficit hawks on the Republican side of the aisle simply disappeared into the walls of Congress.*

But there’s a second, perhaps even more important, angle we need to take into account: wealthy individuals and large corporations—the chief beneficiaries of the Tax Cuts and Jobs Act—would rather lend money to the government, at interest, than pay taxes on the surplus they receive. As federal deficits and debt grow, they end up receiving, not paying for, a larger and larger share of federal expenditures.

I have illustrated the structure of federal debt over time in the chart above. By the end of 2017, the federal debt (the red line) had reached $20 trillion, of which $14.5 trillion was held by the public (the green line).** Private investors (the blue line) own the bulk of debt held by the public (about 83 percent), while foreign investors (both private and public, the yellow line) hold less than half (43 percent) of U.S. public debt.

As we can see, private holders of U.S. public debt—mostly wealthy individuals and large corporations—the majority of whom are based in the United States, are the ones who stand to gain. They have been granted lower tax rates and, at the same time, will receive a mounting share of the interest that is paid out on the growing debt ($310 billion for fiscal year 2018).

In the current political economy of the United States, nothing can be said to be certain, except growing debt payments and lower taxes—all for the benefit of wealthy individuals and large corporations.

*But, as Michael Hiltzik [ht: sm] explains, the species of Republican economists and politicians who aim to cut entitlements, such as Medicare and Social Security, is still thriving.

One would have thought that after saddling the U.S. economy with a tax cut costing $1.5 trillion over 10 years, conservatives and their patrons in corporate America would soft-pedal the usual attacks on Social Security, Medicare and Medicaid.

One would be wrong.

**The difference between federal debt and debt held by the public is made up of intergovernmental holdings, Government Account Series securities held by government trust funds, revolving funds, and special funds (as well as Federal Financing Bank securities).